Losing your job is stressful enough. Having outstanding loans on top of it can feel paralysing. But UAE law is actually on your side here — banks are legally required to support borrowers facing financial difficulty.

You have options. Here’s exactly what they are and how to use them.

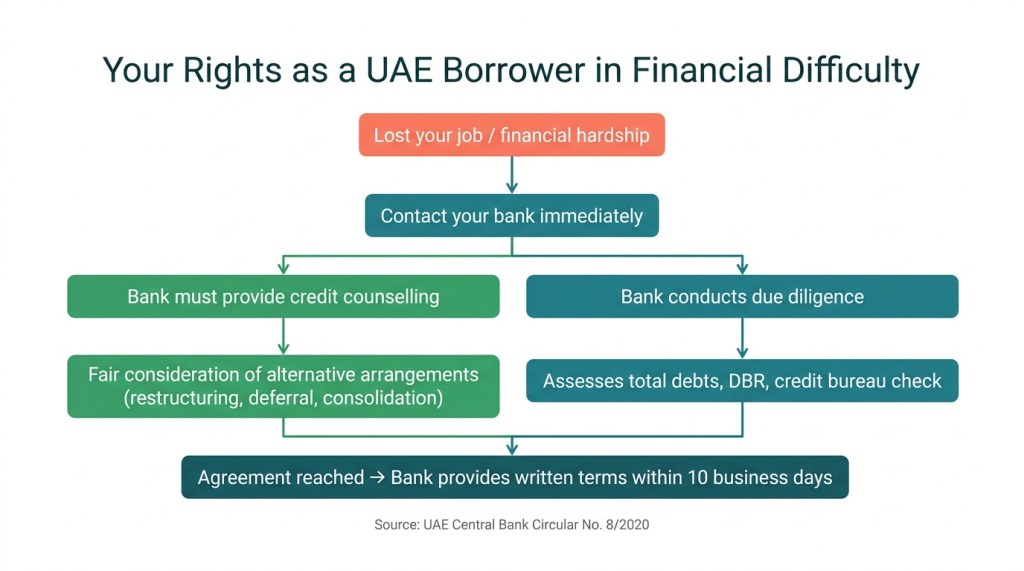

Key Takeaway: Under UAE Central Bank Consumer Protection Standards (Circular No. 8/2020), banks must provide credit counselling, give fair consideration to alternative repayment arrangements, and offer transparent revised terms within 10 business days of reaching an agreement. You are not powerless — the regulatory framework requires banks to work with you.

What Does UAE Law Say About Borrowers in Financial Difficulty?

The UAE Central Bank’s Consumer Protection Regulation (Circular No. 8/2020) sets clear obligations for banks when borrowers face repayment challenges.

Under Article 5.2.4.1, licensed financial institutions must:

- Provide borrowers with qualified credit counselling on debt problems

- Encourage borrowers to feel confident about approaching the bank openly

- Give reasonable consideration to alternative arrangements that could help borrowers overcome repayment difficulties

This isn’t optional guidance. It’s a regulatory requirement. If you approach your bank about repayment difficulties, they are obliged to engage with you constructively.

What Options Can You Request?

When you contact your bank, you can request several types of relief:

Loan restructuring — Extending your repayment period to reduce monthly instalments. This keeps the total loan amount the same but spreads it over more time.

Loan rescheduling — Adjusting the payment dates or frequency to match your changed financial situation.

Payment deferral — Temporarily pausing payments for an agreed period. Some UAE banks are already offering deferrals of up to three months for eligible customers during the current regional disruption.

Loan consolidation — Combining multiple loans into a single facility with one monthly payment, potentially at a lower rate.

Interest/profit rate adjustment — Negotiating a reduced rate for the restructured period.

The bank will assess your eligibility based on your total debt obligations, remaining assets, and the Central Bank’s Debt Burden Ratio (DBR) requirements.

What Happens After You Reach an Agreement?

Under Article 5.2.4.4 of the Consumer Protection Regulation, once you and your bank agree on revised terms, the bank must — within 10 business days — provide you with:

- A written document clearly explaining the revised repayment arrangement

- A detailed payment schedule showing how each payment is allocated between interest/profit and outstanding balance

- Disclosure that any arrears information will be reported to the Credit Information Agency (Al Etihad Credit Bureau)

This last point is important. Even with a restructured loan, any missed payments that occurred before the restructuring will remain on your credit record. Get the revised agreement in writing before stopping or changing payments.

What Will the Bank Check Before Approving?

Under Article 7.1.4.8, banks must conduct due diligence on your overall financial position before restructuring. This includes:

- Your total outstanding debt — both secured (mortgage, car finance) and unsecured (personal loans, credit cards)

- Verification with the Credit Information Agency

- Assessment of your Debt Burden Ratio — the percentage of your income going to debt repayments

If you’ve lost your job, the bank will factor in your end-of-service gratuity, any savings, and your realistic prospects for re-employment.

Be upfront about your full financial picture. Banks are more likely to offer favourable terms when borrowers are transparent rather than defensive.

Step-by-Step: How to Approach Your Bank

- Contact your bank immediately. Don’t wait until you miss a payment. Proactive borrowers get better treatment than defaulting ones.

- Prepare your documents. Bring your employment termination letter, most recent salary certificate, bank statements showing existing obligations, and any MOHRE documentation related to your employment status.

- Request a formal meeting with the credit counselling or collections department — not a general customer service agent.

- Ask for specific options in writing. Don’t accept verbal promises. The law requires banks to provide written terms within 10 business days of any agreement.

- Review the revised schedule carefully. Check how payments are split between interest and principal. Confirm the total cost over the revised term — sometimes extending a loan significantly increases total interest paid.

- Get independent advice if needed. The UAE offers legal protections for borrowers in difficulty, and consulting a financial adviser before signing restructured terms is worth the investment.

Can Banks Refuse to Help?

Banks cannot ignore your request. The Consumer Protection Regulation requires them to give “reasonable consideration” to alternative arrangements.

However, approval isn’t guaranteed. If your debt burden is already at the Central Bank’s maximum ratio, or if the bank assesses that restructuring still won’t result in sustainable repayments, they may offer limited options.

In such cases, you may need to explore:

- Selling assets to reduce the principal balance

- Negotiating a settlement for less than the full amount owed (rare, but possible for unsecured debt)

- Seeking court-ordered instalment plans — UAE courts can grant structured repayment orders based on your financial capacity

What About Your Credit Score?

Any restructuring or rescheduling will be reported to the Al Etihad Credit Bureau. This may affect your credit score, though the impact varies:

- A restructured loan with agreed terms is viewed more favourably than a defaulted loan

- Maintaining payments under the revised schedule will gradually rebuild your credit profile

- Arrears before restructuring will remain on your record for a defined period

Protecting your credit matters — especially if you plan to continue living and working in the UAE. Future employment, visa applications, and financial services all reference your credit history.

What If You’re Planning to Leave the UAE?

Leaving the country does not cancel your debt obligations. Under Article 721 of the UAE Civil Transaction Code, borrowers must repay loans regardless of changes in circumstances.

Banks can pursue debt recovery through legal channels, including travel bans and court orders. If you’re considering departure, negotiate a settlement or structured repayment plan before leaving — it’s far harder to resolve from abroad.

FAQ

Can I defer loan payments if I lose my job in the UAE?

Yes. You can request payment deferrals from your bank. UAE Central Bank regulations require banks to give fair consideration to alternative repayment arrangements for borrowers in financial difficulty.

Is my bank legally required to help me renegotiate?

Banks are required to provide credit counselling, encourage open discussion about financial concerns, and give reasonable consideration to alternative arrangements. However, approval of specific terms depends on the bank’s assessment of your financial situation.

How long does the bank have to provide revised terms?

Under Article 5.2.4.4 of the Consumer Protection Regulation, banks must provide a written document explaining revised repayment terms within 10 business days of reaching an agreement.

Will loan restructuring affect my credit score?

Yes. Any restructuring, rescheduling, or arrears will be reported to the Al Etihad Credit Bureau. However, a restructured loan with maintained payments is viewed more favourably than a default.

What documents do I need to bring to the bank?

Prepare your employment termination letter, most recent salary certificate, bank statements, details of all outstanding debts, and any MOHRE documentation related to your employment status.

Can I consolidate multiple loans into one?

Yes. Loan consolidation is one of the options you can request. The bank will assess your eligibility based on total debt obligations and the Central Bank’s Debt Burden Ratio requirements.

What is the Debt Burden Ratio?

The DBR is the percentage of your monthly income allocated to debt repayments. The UAE Central Bank sets maximum DBR limits that banks must follow when assessing loan applications or restructuring requests.

Can I negotiate a reduced settlement amount?

Settlement for less than the full amount owed is uncommon but possible, particularly for unsecured debts where the bank assesses recovery prospects as limited. This is a negotiation — there’s no automatic right to a reduced settlement.

What happens if I leave the UAE with unpaid loans?

Your debt obligations remain enforceable. Banks can pursue legal remedies including travel bans and court orders. Resolving debts before departure is strongly recommended.

Should I stop making payments while negotiating?

No. Continue making payments until a revised agreement is confirmed in writing. Stopping payments without formal approval can trigger penalties, default proceedings, and negative credit reporting.

Leave a comment