Key Takeaway: Moody’s Ratings forecasts that UAE property prices — particularly mid-market apartments — will soften over the next 12 to 18 months as 180,000 new units complete in Dubai between 2026 and 2028. That’s roughly 60,000 units per year, nearly double the historical average. Developers are expected to scale back new launches, though strong population growth and high-net-worth migration will prevent a sharp correction.

Five years of record-breaking price growth in Dubai’s property market are heading into a new phase. And for the first time in a while, the shift is likely to favour buyers.

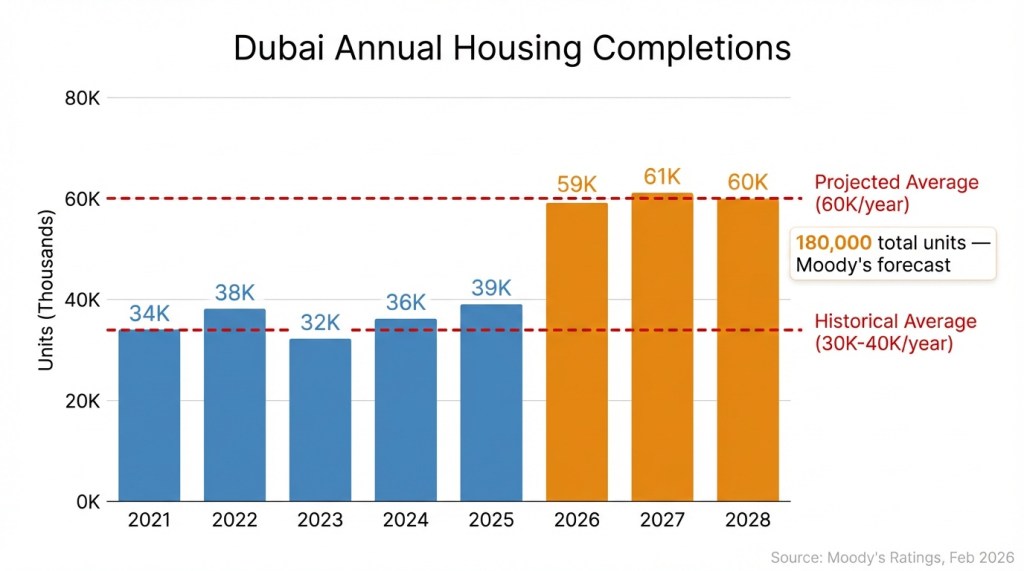

Moody’s Ratings has issued its latest assessment of the UAE real estate sector, and the headline figure is hard to miss: 180,000 new residential units will be completed in Dubai between 2026 and 2028. That averages approximately 60,000 units annually — significantly above the historical delivery rate of 30,000 to 40,000 units per year over the past five years.

The result? Slower price growth, some outright declines in specific segments, and a market that finally starts to rebalance after half a decade of extraordinary gains.

What Exactly Is Moody’s Predicting?

Moody’s analysts are measured in their language. This is not a crash prediction. The agency forecasts modest price softening across the broader market, with the most visible declines expected in the apartment segment — specifically mid-market studios and one-bedroom units where new supply is most concentrated.

“Modest outright price declines are probable in the apartment segment, especially within the more affordable mid-market studio and one-bedroom categories, where supply remains elevated,” the agency stated.

The slowdown is expected to push developers to scale back new project launches, leading to lower new sales values over the next 12 to 18 months. Moody’s indicated this moderation will “persist for several years.”

This aligns with earlier forecasts from Fitch Ratings, which projected a potential 15% correction beginning in late 2025 or early 2026 due to the supply-demand imbalance.

Why 180,000 Units Changes the Equation

Context matters here. Between 2021 and 2025, Dubai’s property market operated in an environment of relatively tight supply against surging demand. That dynamic powered a roughly 60% price increase across residential property since 2022.

The incoming wave of 180,000 completions is a structural shift. At 60,000 units per year, that’s nearly double the supply the market has absorbed annually in recent years.

Moody’s notes that sustained population growth and a shift toward smaller household sizes will help absorb a significant portion of this supply. But even with absorption, the sheer volume of new units entering the market will slow price momentum — particularly in areas already saturated with new development inventory.

For tenants, this supply wave is promising. Rent stabilisation trends already visible in 2025 are likely to accelerate as more units compete for occupancy.

Who Gets Hit Hardest?

Not all property types face the same pressure.

Mid-market apartments — studios and one-bedroom units in the affordable to mid-range segment — bear the greatest risk. These are the categories where developers have concentrated the most supply, and where buyer competition will be fiercest.

Luxury and villa segments are better insulated. Moody’s points to the continued influx of high-net-worth individuals as a supporting factor for premium property. The Dubai rent forecast for 2026 already noted that supply-constrained areas like Palm Jumeirah and Downtown Dubai would see stronger performance compared to areas receiving mass handovers.

Investors with off-plan purchases in mid-market communities should watch delivery timelines closely. Communities with the highest concentration of new units may experience price compression upon handover.

Developers Are Still Financially Strong

Here’s what keeps this from being a crisis story. Moody’s notes that rated developers’ credit quality will remain resilient, supported by:

- Strong revenue backlogs built from aggressive sales since 2021

- Front-loaded payment plans that have already collected cash from buyers

- Solid financial positions with reduced leverage

Emaar’s revenue backlog alone reached Dh127 billion by Q1 2025 — a 62% year-on-year increase. This financial buffer means major developers can maintain delivery schedules even as sales moderate.

However, Moody’s warned that smaller developers remain more exposed to funding and execution risks. Those without the same revenue backlog protection could face pressure if new sales decline materially.

Why UAE Developers Are Looking Overseas

One of the more significant signals from the Moody’s report is the pivot toward geographic diversification.

The ratings agency projects that strong cash generation over the next two to three years by UAE developers “will exceed domestic reinvestment opportunities as new sales moderate.” In simpler terms: developers will have more cash than viable projects at home.

This is already happening. UAE-based developer Arada expanded into the Australian property market last year, establishing a Sydney office and planning multiple projects in New South Wales.

The funding sources are in place. UAE developers have issued close to $12 billion in sukuk, bond, and hybrid debt since 2023, supplemented by customer instalments on off-plan projects and joint ventures with landowners.

Moody’s cautioned that while financial positions remain strong, “sustained cash extraction could gradually weaken local operating companies.” The diversification strategy carries execution risk, particularly for developers expanding into unfamiliar markets.

What This Means for Buyers and Investors

If you’ve been priced out of Dubai’s property market over the past few years, the next 12 to 18 months may present better entry points — particularly in the mid-market apartment segment.

For current property owners, this is not a sell signal. Moody’s describes a modest correction, not a structural decline. Population growth, high-net-worth migration, and the Dubai First Home Initiative continue to support demand fundamentals.

For investors in off-plan properties nearing handover, pay attention to which communities are receiving the most supply simultaneously. Concentrated delivery in a single area can suppress rental yields and resale values in the short term.

FAQ

Will Dubai property prices crash in 2026?

No. Moody’s forecasts a modest decline, not a crash. Strong population growth, high-net-worth migration, and developer financial resilience support the market. The correction is expected primarily in mid-market apartments where supply is highest.

Which property types are most at risk of price declines?

Mid-market studios and one-bedroom apartments face the greatest pressure. These categories have the highest concentration of new supply entering the market between 2026 and 2028.

How many new units are being delivered in Dubai?

Approximately 180,000 new residential units will complete between 2026 and 2028, averaging 60,000 units per year. This nearly doubles the historical average of 30,000 to 40,000 annual deliveries.

Are luxury properties affected by the forecast?

Luxury and villa segments are better protected due to limited supply and continued demand from high-net-worth individuals relocating to the UAE. Price softening is expected to be concentrated in the more affordable categories.

Why are UAE developers expanding overseas?

Moody’s notes that cash generation will exceed domestic reinvestment opportunities as new sales moderate. Developers like Arada have already entered markets such as Australia, while strong financials from $12 billion in debt issuance since 2023 support international expansion.

Is now a good time to buy property in Dubai?

The next 12 to 18 months may offer improved pricing in mid-market segments as new supply enters the market. However, timing depends on individual circumstances, property type, and location. Areas receiving concentrated handovers may present the most favourable negotiating conditions.

Will rents decrease in Dubai?

Moody’s expects the supply increase to moderate rental growth. Areas with significant new inventory may see stabilisation or declines, while supply-constrained neighbourhoods are likely to maintain rental pressure.

Further Reading

- UAE Property Prices Drop 2026: 150,000 New Homes Coming

- Dubai Property Prices Set for 15% Drop — Fitch Report

- Dubai Property Market: 243,000 New Homes to Stabilise Prices by 2027

- Dubai Rent Forecast 2026: Up to 6% Increase Expected

- Dubai Rent Prices Stabilising in 2025: Slowdown in Key Areas

- Dubai First Home Initiative: $1.36m Cap & 18-Year Terms

Leave a comment