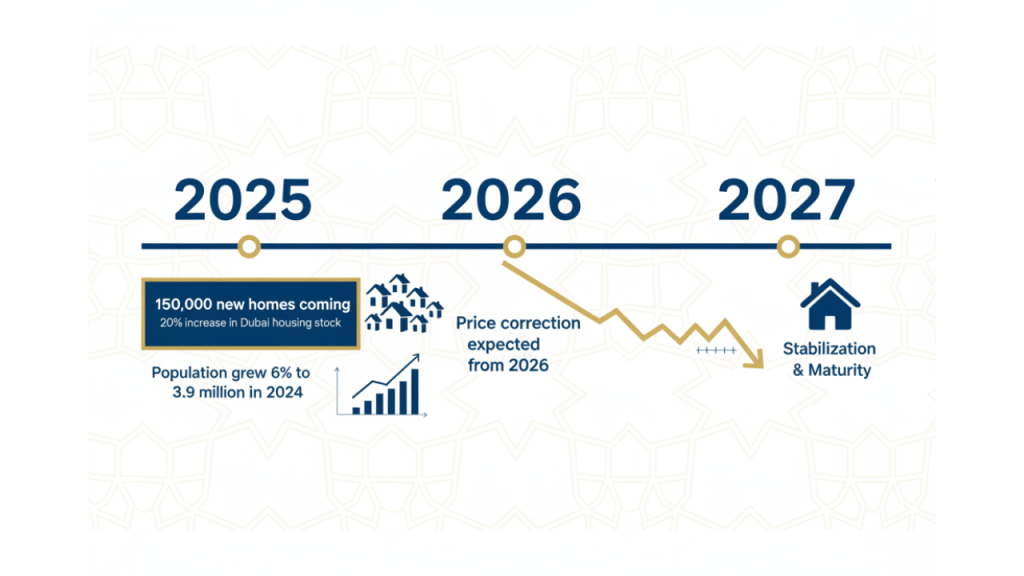

The UAE property market is approaching a significant shift, with Moody’s Ratings predicting price corrections beginning in 2026 as an unprecedented wave of new housing supply reaches the market. This transformation promises to reshape the landscape for buyers, renters, and investors across the Emirates.

The Supply Surge: 150,000 New Homes Coming

Over 150,000 new residential units are scheduled for delivery between 2025 and 2027, representing approximately 20% growth in Dubai’s existing housing stock. This substantial increase in supply forms the foundation of Moody’s forecast for “a modest price correction starting in 2026.”

The timing couldn’t be more significant for residents who have weathered years of rising property costs and rental increases. This supply injection represents one of the largest housing expansions in the UAE’s recent history.

What Residents Can Expect

For property buyers: Increased bargaining power and more diverse options across different price segments

For renters: Potential relief from steep rental increases that have characterised recent years

For investors: A more balanced market with opportunities in specific segments

The correction doesn’t signal market collapse but rather a healthy rebalancing after years of rapid growth.

Demand Fundamentals Remain Strong

Despite the anticipated price moderation, underlying demand drivers continue to strengthen. Dubai’s population expanded 6% in 2024, reaching 3.9 million residents, supported by robust economic growth and progressive visa policies.

Changing household dynamics also contribute to housing demand. Average household sizes have decreased from 4.4 people in 2019 to 3.9 people currently, creating additional demand for housing units even without population growth.

The wealthy demographic influx adds another layer of market complexity. Dubai now hosts over 80,000 millionaires—double the number from a decade ago. In the first quarter of 2025 alone, more than 590 homes priced above Dh20 million changed hands, marking the highest luxury sales volume in two years.

Villa vs Apartment Market Dynamics

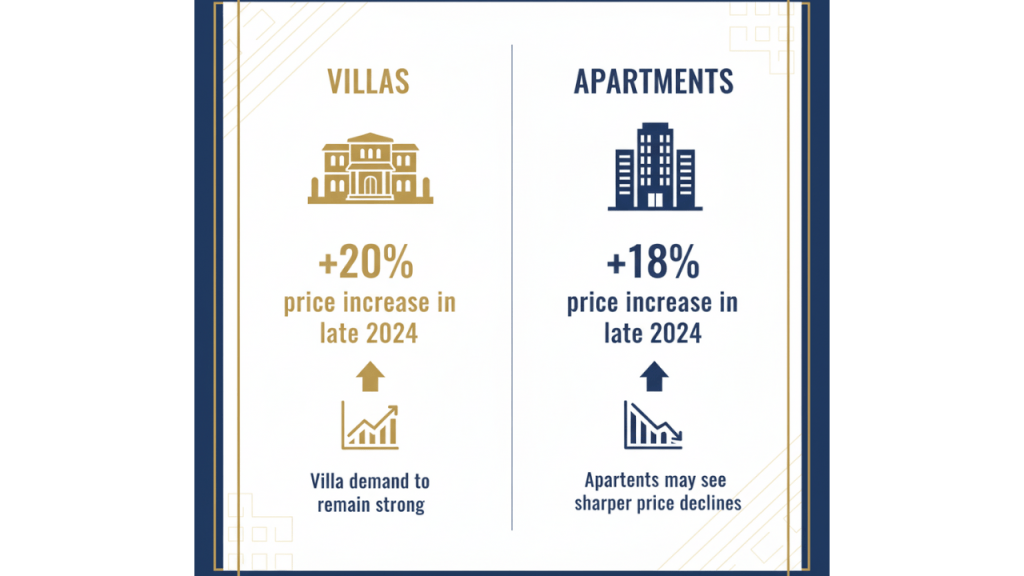

Property type significantly influences market trajectories. Villa prices climbed 20% in late 2024 compared to the previous year, while apartments increased 18% during the same period.

Villa market outlook: Strong demand expected to continue in the near term, though growth rates will moderate as new communities launch

Apartment market forecast: Mid-market apartments may experience sharper price declines once supply exceeds demand, potentially offering better value for buyers

This divergence creates distinct opportunities across different property segments and price points.

Developer Financial Strength Provides Stability

Current market conditions differ markedly from previous cycles due to improved developer financial health. Major builders have significantly strengthened their balance sheets:

- Emaar’s revenue backlog: Increased from Dh25 billion in 2020 to Dh129 billion in 2025

- Average developer leverage: Decreased from 4.8x in 2020 to 1.4x in 2025

- Combined profits: The six largest developers generated Dh46 billion in the past year, up from Dh12 billion five years earlier

This financial stability means developers can maintain project delivery schedules even if market conditions soften, providing greater certainty for buyers and the broader market.

Enhanced Buyer Protection Measures

Regulatory improvements over the past decade have created a more secure environment for property purchasers. Key protections include:

Escrow account requirements: Off-plan buyer funds must be held in escrow, released only when construction milestones are achieved

Stricter launch requirements: Developers must secure land and approvals before initiating sales

Expanded regulatory coverage: Sharjah introduces new escrow legislation this year, aligning protections with Dubai and Abu Dhabi standards

These measures safeguard individual buyers while supporting long-term market stability by reducing systemic risks.

Strategic Considerations for Different Market Participants

Property buyers should prepare for increased choice and potentially more favourable pricing from 2026, particularly in the apartment segment.

Rental tenants may benefit from supply-driven rent stabilisation, especially in mid-market apartment categories.

Property investors should note that villa and luxury segments maintain strong demand, though competition is intensifying rapidly.

The market outlook suggests stability rather than volatility, with Moody’s emphasising that fundamental demand drivers support continued market health despite increased supply.

Key Takeaway: The UAE property market is entering a rebalancing phase from 2026, with 150,000 new homes creating more choice for buyers and rent stability for tenants, while strong demand fundamentals and improved developer finances maintain overall market stability.

Frequently Asked Questions

Q: Will UAE property prices crash in 2026? A: Moody’s forecasts a “modest price correction,” not a crash. Strong population growth and millionaire immigration continue supporting demand.

Q: Should I wait until 2026 to buy property in Dubai? A: The 150,000 new homes will create more choice and potential bargaining power, particularly for apartments in mid-market areas.

Q: Which property types will see the biggest price changes? A: Mid-market apartments may see sharper declines, while villas and luxury properties are expected to maintain stronger demand.

Q: Are UAE property developers financially stable? A: Yes, major developers have significantly reduced debt levels and increased profits, with average leverage dropping from 4.8x to 1.4x since 2020.

Leave a comment