The United Arab Emirates has taken a groundbreaking step in digital finance by officially recognising the Digital Dirham as legal tender. Federal Decree Law No. 6 of 2025 places this digital currency on the same legal footing as physical cash, defining the Dirham as being represented by “notes, coins and digital forms.”

Direct Answer: Yes, you will be able to receive your salary in Digital Dirhams once the Central Bank of the UAE finalises implementation regulations. The new law recognises Digital Dirham as legal tender for “payment of any amount,” meaning no merchant, financial institution, or public body will be permitted to refuse it for goods or services—including salary payments.

What Is the Digital Dirham and How Does It Work?

The Digital Dirham represents a digital version of the UAE’s national currency, backed by the Central Bank of the UAE (CBUAE). Unlike cryptocurrency, this is a Central Bank Digital Currency (CBDC) that carries the full trust and security of traditional central bank-backed money.

The pilot phase has already begun. On Tuesday, the Ministry of Finance and Dubai’s Department of Finance completed the UAE’s first government financial transaction using Digital Dirham, coordinating with the CBUAE. This demonstration formed part of efforts to accelerate digital payment adoption across the Emirates.

According to a CBUAE policy paper, the Digital Dirham aims to simplify payment processes by reducing transaction costs and enabling immediate settlement for retail, wholesale, and cross-border payments.

Can Employers Pay Salaries in Digital Dirhams?

Ali Awad, Partner at Al Tamimi & Company, confirms that salary payments in Digital Dirham are legally possible under the new framework.

“Legally, now that the Digital Dirham is recognised as legal tender, there is no legal obstacle to paying salaries, retail purchases, or remittances in Digital Dirhams,” Awad explained.

However, operational implementation requires additional steps. The CBUAE Board of Directors must first issue detailed implementation regulations governing how the digital currency will be issued, circulated, redeemed at full nominal value, and legally transferred.

UAE employers will need to integrate their salary payment systems with Digital Dirham infrastructure. This includes wallet interoperability and compatibility with the existing Wage Protection System (WPS) that currently governs salary payments in the UAE.

Point-of-sale networks and remittance platforms will also require system upgrades to accept Digital Dirham transactions. Public and private sector readiness to accept Digital Dirhams will be essential, alongside cross-border agreements with foreign regulators to enable international remittances via CBDC corridors.

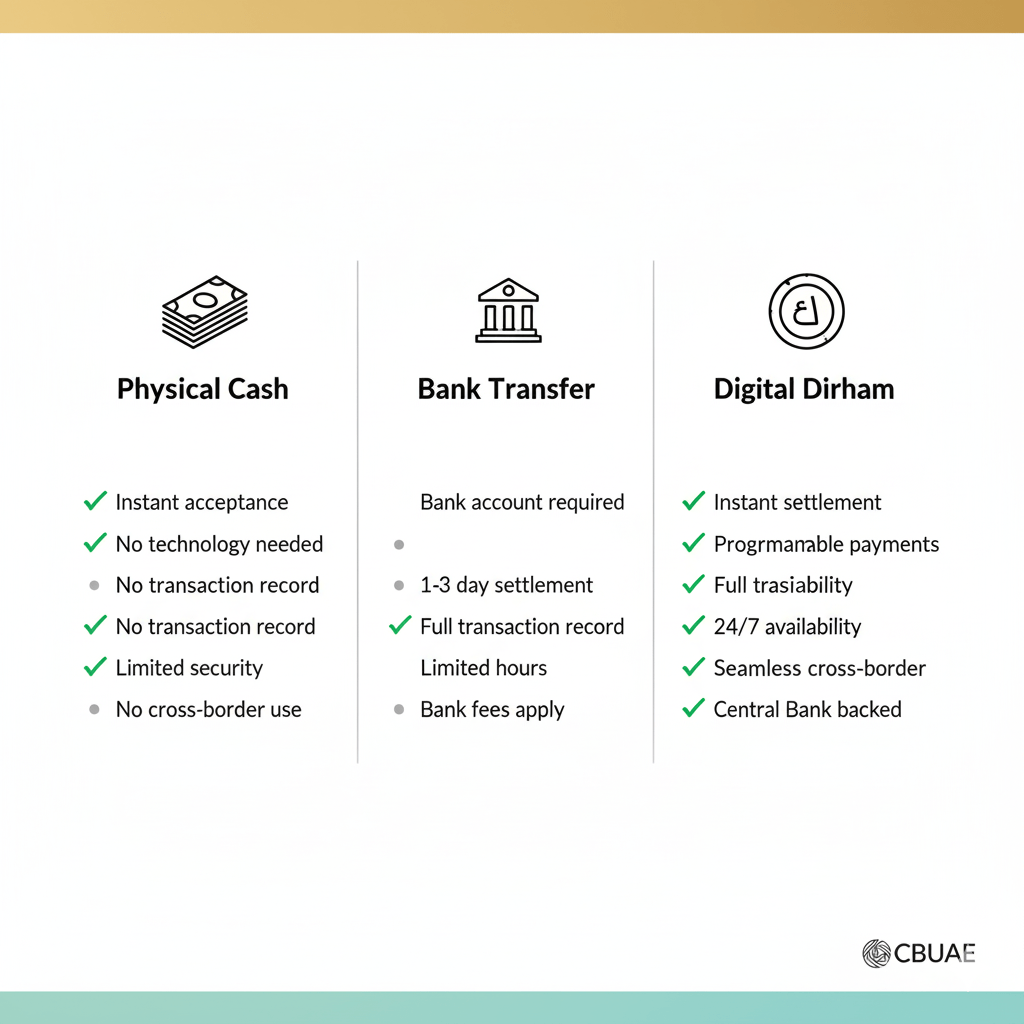

How Is Digital Dirham Different from Cash and Bank Transfers?

The Central Bank describes the Digital Dirham as enabling “instant settlements and widespread accessibility with the security and trust of traditional central bank-backed money.” However, it offers several advantages over both physical cash and traditional bank transfers.

Key Differences:

Unlike cash, the Digital Dirham supports programmable payments, real-time settlement, and seamless cross-border transfers. These capabilities require updated infrastructure and compliance protocols across UAE’s banking sector.

The digital currency will be treated as equivalent to central bank reserves, prompting changes in liquidity management, regulatory treatment, and access to CBUAE facilities. This differs significantly from commercial bank deposits or digital wallets currently used for money transfers.

“Designed for retail, wholesale, and international use, the Digital Dirham aims to enhance payment system efficiency and strengthen monetary policy execution,” Awad explained.

A widely accessible CBDC could also broaden financial inclusion by giving unbanked or underbanked individuals easier access to formal financial services—an important consideration for UAE’s diverse workforce.

How Will You Access Digital Dirhams?

The CBUAE plans to roll out the Digital Dirham in phases, with risk controls built into its design from the start.

The distribution model uses what the Central Bank calls “an intermediated CBDC model, with hybrid wallet-based access.” This means you won’t download an app directly from the Central Bank. Instead, Digital Dirham wallet providers will include:

- Licensed Financial Institutions (LFIs): Traditional banks, exchange houses, and payment service providers

- FinTech Companies: Those holding Store Value Facility (SVF) licences

This approach is similar to how Al Ansari Financial Services and other exchange houses currently operate digital payment services.

The Digital Dirham relies on a hybrid architecture that combines account- and token-based elements. Users will hold wallets with account identifiers, while all transactions will be recorded on a permissioned distributed ledger. This provides both the convenience of digital payments and the security of blockchain-style transaction recording.

What About Cross-Border Payments and Remittances?

One of the most significant advantages of Digital Dirham is its potential to transform international money transfers—a crucial feature for the UAE’s large expatriate workforce.

The UAE leads the GCC in remittance outflows, with billions of dirhams sent internationally each year. Currently, these transfers can take 2-5 business days and incur various fees.

Digital Dirham could dramatically change this landscape through CBDC corridors—agreements between central banks that allow direct digital currency transfers between countries. These corridors would enable instant, low-cost international remittances without the need for correspondent banking networks.

However, implementation requires “cross-border agreements with foreign regulators to enable international remittances via CBDC corridors,” according to legal experts. These bilateral agreements are currently under development with several countries.

For workers sending money home through traditional remittance channels, Digital Dirham could eventually offer a faster, cheaper alternative—though the timeline depends on international regulatory cooperation.

Regulatory Framework and Enforcement

The Digital Dirham framework forms part of a wider overhaul introduced under Federal Decree Law No. 6 of 2025. This legislation consolidates the regulation of banks, insurers, and FinTech companies under the Central Bank.

The law introduces stronger enforcement tools to support the digital currency ecosystem:

- Early-intervention powers for the Central Bank

- Administrative fines of up to AED 1 billion for serious breaches

- Comprehensive regulatory oversight of digital currency operations

These enforcement mechanisms demonstrate the UAE’s commitment to maintaining a secure and reliable digital currency system. The Central Bank’s regulatory approach balances innovation with consumer protection and financial stability.

Timeline and Implementation Phases

The CBUAE has confirmed it will implement the Digital Dirham in phases, though specific timelines for each phase have not been publicly announced.

The pilot phase is already underway, with the Ministry of Finance and Dubai’s Department of Finance completing the UAE’s first government transaction using Digital Dirham. This test transaction validated the technical infrastructure and operational procedures needed for larger-scale deployment.

Industry sources suggest that detailed implementation regulations from the CBUAE Board of Directors are “still pending.” These regulations will need to cover:

- Issuance procedures for Digital Dirhams

- Circulation mechanisms through licensed providers

- Redemption processes at full nominal value

- Legal transfer requirements and protocols

- Wallet interoperability standards

- Transaction recording and verification procedures

Once these regulations are finalised and the system becomes operational, the framework will become mandatory for all participants in the UAE’s financial ecosystem.

Impact on Banking and Financial Services

The introduction of Digital Dirham as legal tender will significantly impact UAE’s banking sector and financial services industry.

Banks will need to adapt their systems to accommodate Digital Dirham alongside traditional banking services. This includes integrating digital currency capabilities into existing platforms, training staff on new protocols, and updating customer service procedures.

For UAE’s growing FinTech sector, the Digital Dirham presents both opportunities and challenges. Licensed FinTech providers with SVF licences can become Digital Dirham wallet providers, opening new revenue streams and customer acquisition channels.

The financial services job market will likely see increased demand for professionals with expertise in:

- Digital currency operations

- Blockchain technology

- Payment system integration

- Regulatory compliance for digital assets

- Cybersecurity for digital financial services

Salaries in the financial services sector may reflect this increased specialisation, particularly for roles involving Digital Dirham infrastructure development and management.

What This Means for UAE Residents and Businesses

For individuals living and working in the UAE, Digital Dirham will eventually offer more payment options and potentially lower transaction costs.

Retail shopping could become more convenient through instant digital payments that don’t require physical cash or bank card processing delays. Freelancers and self-employed professionals may find Digital Dirham particularly useful for invoicing and receiving payments.

Businesses operating in the UAE will need to prepare their payment infrastructure for Digital Dirham acceptance. Point-of-sale systems, accounting software, and financial management platforms will require updates or replacements to handle the new currency format.

The UAE’s position as a regional business hub means many companies operate across multiple jurisdictions. Digital Dirham’s cross-border capabilities could simplify international transactions and reduce the complexity of managing multi-currency operations.

FAQ

When will Digital Dirham become available for general use?

The CBUAE has not announced a specific launch date for general availability. The system is currently in the pilot phase, with implementation planned in stages. Detailed regulations must be finalised before widespread rollout.

Will I be forced to use Digital Dirham instead of cash?

No. Digital Dirham will exist alongside physical cash and traditional banking services. However, once operational, merchants and institutions cannot refuse Digital Dirham as payment, just as they cannot refuse physical Dirham notes.

Do I need a bank account to use Digital Dirham?

Not necessarily. The intermediated model allows access through various wallet providers, including banks, exchange houses, and FinTech companies. The specific account requirements will depend on which wallet provider you choose.

How is Digital Dirham different from cryptocurrency like Bitcoin?

Digital Dirham is a Central Bank Digital Currency (CBDC) backed by the UAE government and Central Bank. Unlike cryptocurrency, it’s not decentralised, doesn’t fluctuate in value against the Dirham, and carries the full legal tender status of government-issued currency.

Will Digital Dirham transactions be private?

All Digital Dirham transactions will be recorded on a permissioned distributed ledger. This provides transaction traceability for security and regulatory purposes while maintaining appropriate privacy protections. Specific privacy protocols will be detailed in the implementation regulations.

Can expatriates send Digital Dirhams to their home countries?

Eventually, yes—but only to countries that have established CBDC corridors with the UAE. These require bilateral agreements between central banks. The CBUAE is working on these agreements, but availability will vary by country.

What happens to my Digital Dirhams if the wallet provider shuts down?

Since Digital Dirhams are central bank reserves rather than commercial bank deposits, they should be recoverable even if a wallet provider ceases operations. Specific consumer protection protocols will be outlined in the implementation regulations.

Will there be fees for Digital Dirham transactions?

Transaction fee structures have not been announced. However, one of the stated goals is to reduce transaction costs compared to traditional payment methods. Final fee structures may vary by wallet provider and transaction type.

Further Reading

- UAE Salary Guide 2025: Top In-Demand Jobs and Payment Scales

- Complete Guide to Average Salary in Dubai: 2025 Pay Scales & Benefits

- UAE Money Transfer Without Bank: Digital Wallets & Apps Guide 2025

- UAE Leads GCC Remittance Market: India Receives Record $129.4 Billion

- UAE Fintech Jobs Hit Record High in 2024: Salary Gains & Career Moves

- 13 Major UAE Changes in 2025: New Laws, Tech & Fees You Must Know

Leave a comment