For decades, the UAE stood as a beacon for global talent and investment with one compelling promise: a land where paycheques remained untouched by income tax. This simple proposition, combined with pro-business regulations and world-class infrastructure, transformed a federation of emerging cities into a magnet for international business. Yet as the global economy evolved, so too did the UAE’s approach to taxation.

The End of the Tax-Free Era

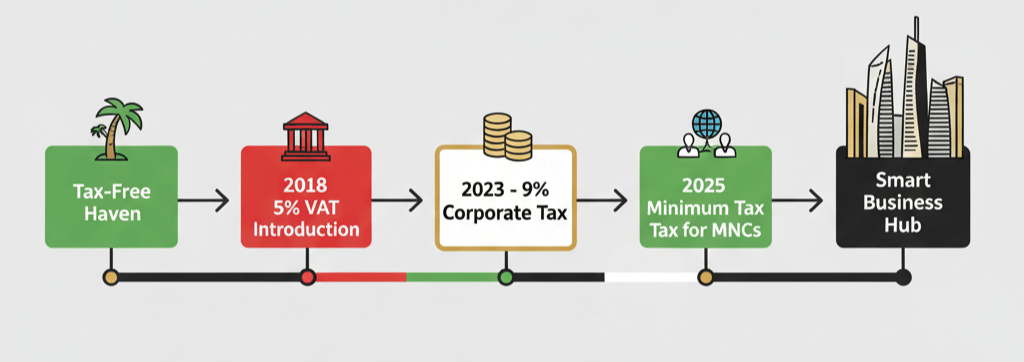

What once was a “tax-free” oasis has become something more sophisticated and strategic. The UAE has systematically introduced a 5% value-added tax, excise duties on harmful products, and most significantly, a 9% corporate tax on business profits. From January 2025, the country implemented a domestic minimum top-up tax of 15% for the world’s largest companies, aligning with OECD global standards.

These changes represent not a retreat from the UAE’s business-friendly approach, but rather an evolution designed to fortify its position as a globally competitive destination for decades to come. The transformation reflects a mature understanding that sustainable economic growth requires both competitiveness and compliance with international fiscal standards.

Corporate Tax Implementation Reality

The real test of this new era arrived on September 30, 2025, when thousands of companies filed their first corporate tax returns. For many businesses, this deadline represented more than a regulatory requirement—it marked a fundamental cultural shift in financial management.

While VAT filing was relatively straightforward, corporate tax demands require a new level of financial discipline. Businesses must measure profits according to international accounting standards, document transactions with related parties, and maintain financial records capable of withstanding regulatory scrutiny.

The choices made in first filings—how revenue is recognised, how expenses are matched—will create ripple effects shaping tax obligations for years. For some organisations, the learning curve has proven steep, but the broader message remains clear: the UAE is transitioning from light-touch administration to full financial maturity.

What Remains Unchanged

Despite these significant fiscal reforms, much about the UAE’s appeal remains familiar. For individuals, there is still no personal income tax—a point the government has repeatedly emphasised. This reassurance matters tremendously to the millions of expatriates who have made the Emirates their home, with tax-free salaries continuing to attract global talent.

VAT, introduced in 2018, has become a settled part of the economic fabric, while excise duties continue nudging consumption habits in healthier directions. What has changed is the depth and sophistication of the overall framework. Corporate tax, though modest by international standards, introduces structures that compel companies to plan, document, and operate with global best practices.

Benefits for Small Businesses

Small businesses receive significant protection under the new system. Profits up to AED 375,000 are shielded from tax, meaning many micro-enterprises owe nothing. Yet the requirement to register and file returns pushes even the smallest firms toward professional standards.

For freelancers and influencers, the system provides flexibility with extended registration deadlines for those earning below AED 1 million annually. The burden may be lighter for small businesses, but the long-term benefit includes enhanced credibility with banks and suppliers.

Over time, even the smallest café or consultancy will find that IFRS-compliant statements open doors to better financing and bigger opportunities. This professional foundation supports startup growth and business expansion across the emirates.

Multinational Corporation Advantages

For multinationals, the new domestic minimum tax ensures compliance with OECD’s global reforms while protecting the UAE’s tax base. Without this proactive approach, profits generated in Dubai or Abu Dhabi could have been taxed elsewhere.

By acting early, the UAE maintains control of its fiscal destiny while demonstrating its commitment to being a serious, rules-based jurisdiction. The appeal for these companies—infrastructure, skilled workforce, time-zone advantages, and lifestyle quality—remains intact, now wrapped in modern regulatory credibility.

The introduction of tax credits for high-value employment provides additional incentives for companies establishing regional headquarters, particularly those employing senior management and core business functions.

Free Zone Clarity and Innovation

Free zones, long the crown jewels of the UAE’s economic model, have received renewed clarity through new ministerial decisions issued in 2025. For years, investors questioned what types of income would qualify for the celebrated zero per cent corporate tax rate.

The refined guidelines expand commodity trading to include environmental products like carbon credits while linking zero-rate benefits to transparent, recognised price benchmarks. By tightening rules, the government preserves free zones’ spirit—encouraging trade, innovation, and sustainability—while deterring abuse.

Companies in free zones like DMCC, Jebel Ali, or DIFC now have confidence that their incentives rest on firm legal ground. The streamlined business setup process continues attracting entrepreneurs and established businesses alike.

Cultural and Operational Transformation

These reforms extend beyond taxation, reshaping business operations throughout the UAE. Under VAT, quarterly reconciliations sufficed; under corporate tax, continuous discipline becomes essential. Monthly closings, rolling forecasts, reconciled balances, and transfer pricing documentation become standard practice.

This cultural shift toward permanence and predictability reassures investors and lenders that financial numbers are reliable. Companies adapting quickly find themselves with competitive advantages: lower borrowing costs, easier access to cross-border markets, and greater stakeholder trust.

The impact has influenced hiring practices, with companies exercising caution in recruitment while managing new tax obligations. However, technology professionals continue commanding premium packages as businesses invest in digital transformation.

Investment and Trust Building

Investors watch closely as the UAE demonstrates a jurisdiction that has outgrown reliance on “tax-free” branding alone. Instead, the country offers something rarer: stability. Tax bases and rates are established in law, not left to discretionary interpretation. Incentives are preserved but tied to legitimate activities.

Enforcement utilises digital, data-driven approaches rather than arbitrary decisions. The message is powerful: this is a place where rules are clear and planning is possible. This transparency allows businesses to make long-term strategic decisions with confidence.

The penalty relief programmes for early corporate tax filers demonstrate the government’s understanding of implementation challenges while encouraging compliance.

Personal Income Tax Speculation

Speculation occasionally resurfaces about whether the UAE might introduce personal income tax. For now, the official answer remains a resounding no. The UAE’s magnetism extends far beyond taxation considerations.

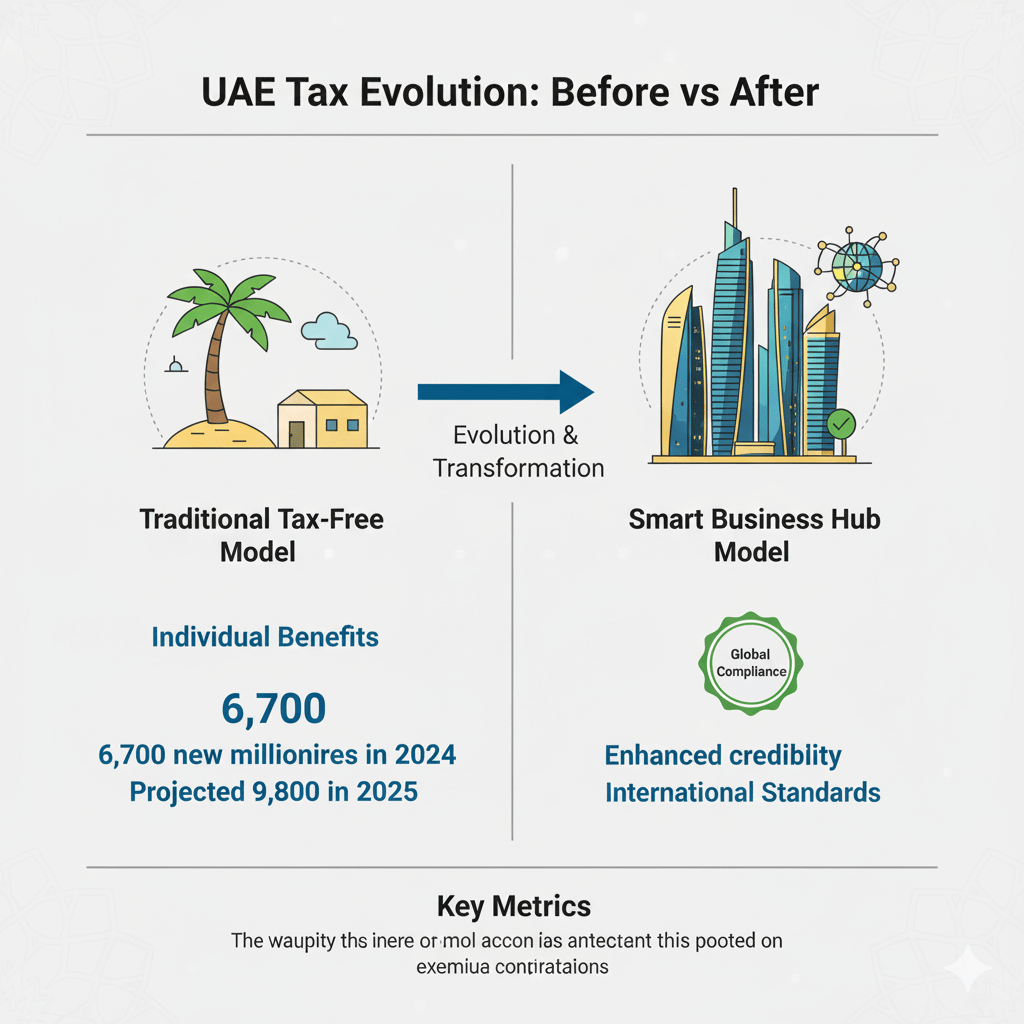

In 2024, the country attracted 6,700 new millionaires—the most globally. Projections for 2025 suggest this number could reach nearly 9,800. They come not just for tax advantages, but for long-term visas, security, connectivity, and a cosmopolitan lifestyle few places can match.

The absence of personal income tax continues supporting the startup ecosystem, with government initiatives training thousands of entrepreneurs while creating substantial employment opportunities.

Data-Driven Insights and Transparency

Perhaps the most transformative benefit of tax reform involves data transparency. Companies now document intercompany pricing, reconcile accounts monthly, and file detailed disclosures, providing regulators and executives sharper insight into economic operations.

This transparency enables lenders to assess risks better, boards to make quicker decisions, and policymakers to design evidence-based incentives. Over time, this cycle of compliance feeding clarity, and clarity fuelling capital, will likely prove one of the most enduring benefits of the UAE’s new fiscal regime.

The digital infrastructure supporting these processes, including VAT refund systems and streamlined business registration platforms, demonstrates the UAE’s commitment to technological innovation in governance.

Future-Proofing the Economy

The UAE is not abandoning its DNA as a pro-enterprise nation; it is upgrading it. By refusing to tax personal income, setting modest corporate rates, implementing global minimums only where necessary, and clarifying free-zone rules, the country builds a system that is both competitive and durable.

This evolution supports the broader economic transformation includes substantial investment in entrepreneurship, technology, and innovation. The balance between maintaining competitive advantages and meeting international standards positions the UAE for sustained growth.

The country is no longer just “low-tax”—it is “high-trust.” For global investors weighing risk and reward, this combination may prove even more attractive than the old promise of tax-free operations.

Key Takeaway

The UAE has entered a new chapter of economic evolution, transitioning from a tax-free haven to a sophisticated, globally compliant business hub whilst maintaining its core competitive advantages. This transformation strengthens rather than weakens the country’s position as a premier destination for international business and talent, offering stability, transparency, and long-term strategic value for investors and entrepreneurs.

Frequently Asked Questions

Has the UAE introduced personal income tax? No, the UAE maintains its commitment to zero personal income tax for individuals. This policy remains unchanged despite corporate tax implementation.

What is the UAE corporate tax rate? The UAE imposes a 9% corporate tax on business profits, with small businesses earning up to AED 375,000 remaining exempt from taxation.

Do free zones still offer tax benefits? Yes, qualifying free zone companies can still benefit from 0% corporate tax rates, though new guidelines have clarified eligible activities and requirements.

When did UAE companies start filing corporate tax returns? The first corporate tax returns were due by September 30, 2025, for companies with financial years ending December 31, 2024.

Are there penalties for late corporate tax registration? Yes, but the UAE has implemented penalty relief programmes, including automatic AED 10,000 refunds for companies that file returns within specified timeframes.

How do these changes affect foreign investment? The reforms enhance the UAE’s credibility as a stable, rules-based jurisdiction whilst maintaining competitive tax rates, potentially making it more attractive for long-term foreign investment.

Further Reading:

- UAE Corporate Tax Guide for Freelancers & Influencers: 2024 Update

- UAE Corporate Tax Refunds: AED 10,000 Penalty Relief Programme

- UAE’s New Corporate Tax Credit: Game-Changer for Global Business HQs

- UAE Free Zone Business Setup: 6 Easy Steps to Success

- UAE Startup Funding Set to Hit $2bn in 2024: Expert Analysis

Leave a comment