Residents earning at least Dh15,000 monthly can now check their home loan eligibility online, as Mashreq launched the UAE’s first fully digital mortgage pre-approval service.

The browser-based service allows salaried applicants to submit details online and receive a verified pre-approval letter on the same day. This helps expatriates determine their borrowing capacity before committing to purchasing property in Dubai or Abu Dhabi.

What Is a Home Loan Pre-Approval?

Srinivasan Padmanabhan, Head of Mortgages at Mashreq, explained that a pre-approval is an “approval in principle” based on the customer’s income, obligations, and profile.

“A final approval is offered once a specific property is selected and the bank completes valuation and remaining checks,” he said.

Can a buyer still be declined after pre-approval? Yes. Padmanabhan confirmed that rejection at the final stage is possible, especially if the customer’s financial situation changes or if any pre-approval criteria are not met.

How the Bank Calculates Your Eligibility

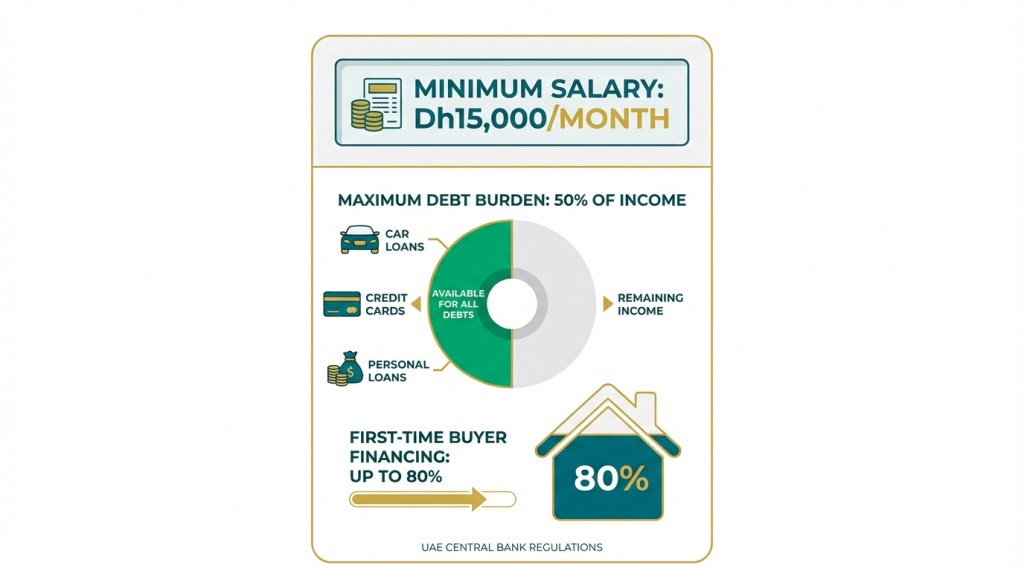

Pre-approval does not look at income alone. The bank considers all liabilities reflected in a customer’s credit bureau report, including:

- Car loans

- Credit cards

- Personal loans

- Other financial commitments

These affect how much a borrower can sustainably repay each month.

Under UAE Central Bank regulations, a customer’s total debt burden cannot exceed 50% of their monthly income—including the home loan instalment being applied for.

For first-time home buyers, salaried expatriates can typically finance up to 80% of the property value. This means a 20% down payment is required.

“From a borrower’s perspective, this approach is designed to prevent over-stretching and support long-term financial wellbeing,” Padmanabhan said.

What Eligibility Actually Means

Padmanabhan defined eligibility as what residents can afford to borrow from a bank to buy their own home. The pre-approval estimates a “responsible loan amount” that the customer can service month on month.

“A mortgage helps customers own their dream homes by paying a small portion upfront (also known as a down payment) and repaying the remainder through manageable monthly instalments,” he said.

“For us, the aim is to give customers early clarity on a realistic budget range—so they can search for homes with complete confidence.”

If you earn Dh15,000 monthly, understanding the cost of living in Dubai helps determine whether homeownership fits your budget.

Documents Required for Digital Pre-Approval

Unlike traditional mortgage processes requiring multiple documents, Mashreq’s digital pre-approval requires only:

- Emirates ID

- Passport

- IBAN (bank account number)

Padmanabhan said this streamlined approach still provides a verified pre-approval that the bank will honour—rather than an indicative calculation based solely on declared information.

What Happens After Pre-Approval?

Once pre-approved, buyers can:

- Shortlist a property

- Sign the memorandum of understanding (MOU)

- Submit property documents to the bank

- Await independent valuation and final approval

Understanding the full costs of buying property in Dubai beyond the purchase price helps avoid surprises during this process.

Is Dh15,000 Enough to Buy Property in Dubai?

A Dh15,000 salary places you at Dubai’s average income level. Whether this income supports homeownership depends on your existing debts and lifestyle expenses.

With the 50% debt burden limit, a buyer earning Dh15,000 with no existing debts could afford monthly loan repayments up to Dh7,500. However, most lenders prefer total obligations below 40% for comfortable approval.

First-time buyers are driving Dubai’s property market, with properties priced between Dh1.2m-Dh3m proving most popular. At 80% financing, a Dh1.2m property requires a Dh240,000 down payment.

Frequently Asked Questions

What is the minimum salary for a home loan in Dubai?

Mashreq’s digital pre-approval service requires a minimum monthly salary of Dh15,000. Other banks may have different thresholds, typically ranging from Dh10,000 to Dh15,000 for expatriates.

How much can I borrow on Dh15,000 salary in Dubai?

Your borrowing capacity depends on existing debts. Under UAE Central Bank rules, total monthly debt payments cannot exceed 50% of your income. With no other debts, this means up to Dh7,500 monthly for all loan repayments combined.

What documents do I need for Mashreq’s digital pre-approval?

Only three documents: Emirates ID, passport, and IBAN. This is significantly fewer than traditional mortgage applications that require salary certificates, bank statements, and employment letters.

Can I still be declined after getting pre-approval?

Yes. Pre-approval is conditional. Final approval depends on property valuation, verification of your financial status at time of purchase, and meeting all original criteria.

What percentage of property value can expatriates finance?

First-time home buyers who are salaried expatriates can typically finance up to 80% of property value. This means a 20% down payment is required.

Does pre-approval guarantee I will get a mortgage?

No. Pre-approval indicates the bank’s willingness to lend based on your current financial profile. Final approval depends on property selection, valuation, and your unchanged financial circumstances.

Leave a comment