Key Takeaway: Zero per cent down payment property purchases are not permitted through bank mortgages in the UAE due to Central Bank regulations requiring minimum buyer contributions. However, developers can offer payment plans that bypass these rules.

You’ve probably seen the offers – “Buy property with zero down payment!” Real estate agents pitch this deal across Dubai, but is it actually legal? The answer depends entirely on how you’re financing your purchase.

What UAE Central Bank Rules Say About Down Payments

The UAE Central Bank has clear regulations about how much money buyers must contribute when purchasing property through a mortgage. These rules exist to protect both buyers and the banking system.

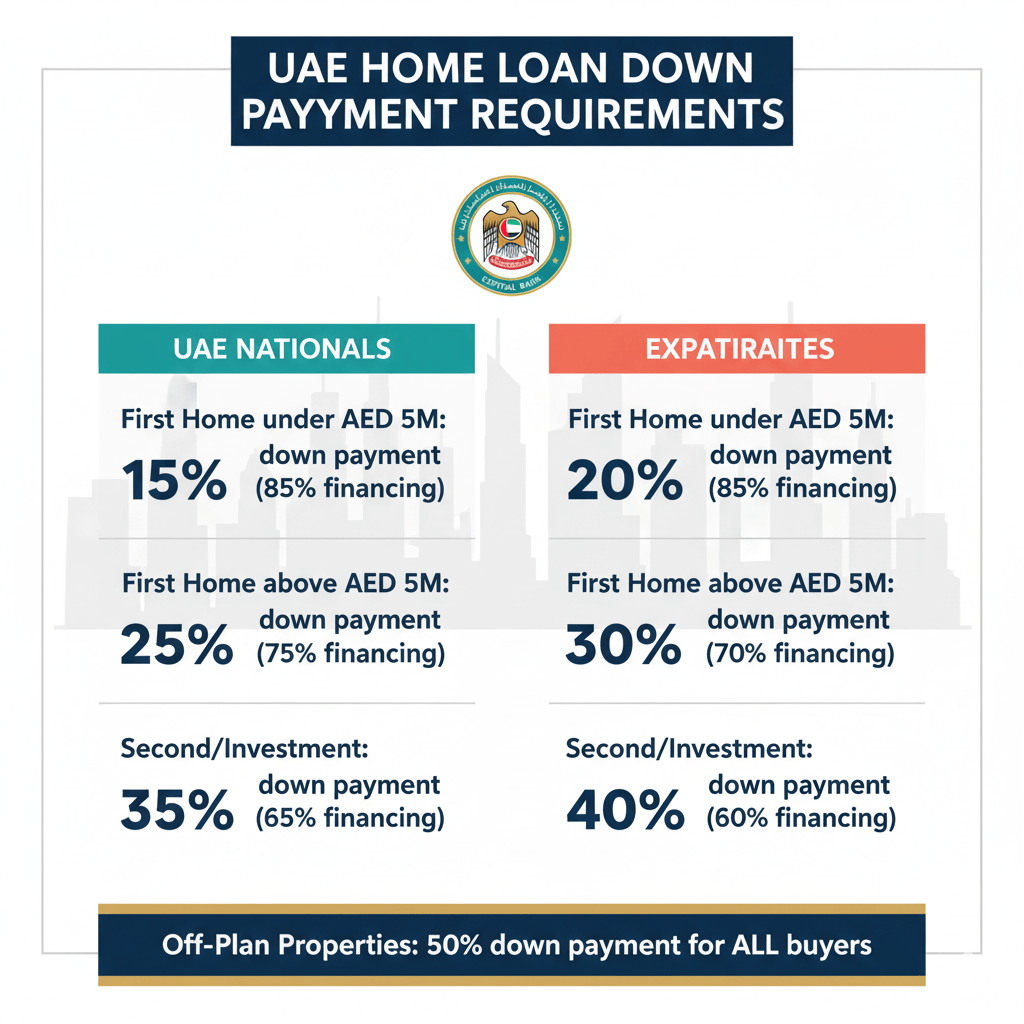

For UAE Nationals:

Your first home has different requirements depending on the property value:

- Properties worth AED 5 million or less: You can borrow up to 85% (meaning a 15% down payment)

- Properties above AED 5 million: Maximum 75% financing (25% down payment required)

- Second homes or investment properties: 65% maximum loan regardless of value

For Expatriates:

The requirements are slightly stricter:

- First property under AED 5 million: 80% maximum financing (20% down payment)

- First property above AED 5 million: 70% financing allowed (30% down payment)

- Additional properties: 60% maximum loan regardless of price

Off-Plan Properties:

These carry higher risk, so the Central Bank caps financing at 50% for everyone – nationals and expatriates alike. This means you’ll need a 50% down payment for off-plan purchases, regardless of the property’s purpose or your nationality.

These regulations come from Notice No. 226/2013 on Mortgage Loans, which remains in effect today.

How Developers Offer Zero Down Payment Legally

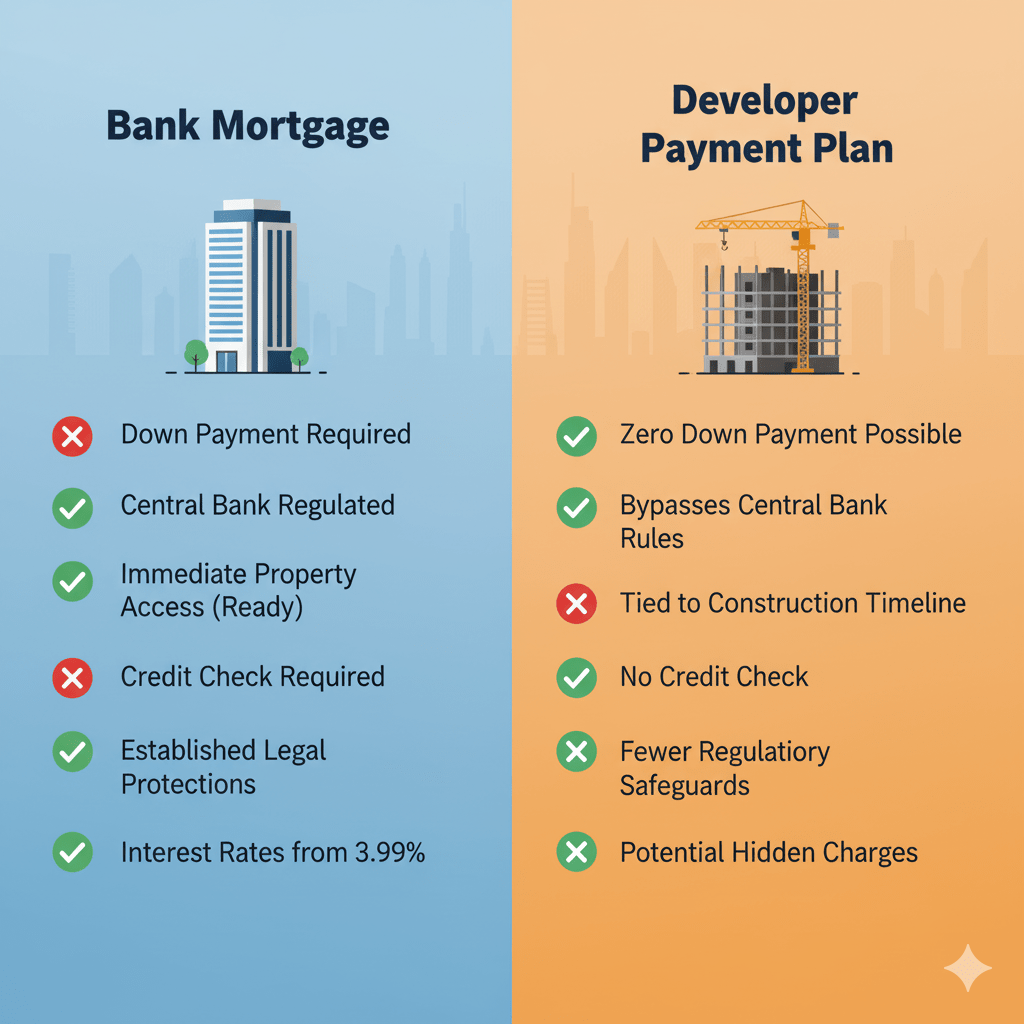

Here’s where it gets interesting. While banks cannot offer zero down payment mortgages, property developers can create their own payment plans that don’t involve traditional bank financing.

Developer payment plans work differently:

- You pay instalments directly to the developer

- No bank mortgage is involved

- The Central Bank mortgage regulations don’t apply

- These plans typically apply to off-plan properties

This explains why you’re seeing zero down payment offers from developers. They’re not breaking any rules – they’re simply offering financing outside the banking system.

What You Need to Watch Out For

Before jumping on a zero down payment offer, understand exactly what you’re signing up for:

Payment Schedule: When do payments start? How much? Over what period? Get this in writing.

Handover Terms: What happens if the project is delayed? What are your rights? Dubai has strong protections for off-plan buyers, but you need to understand them.

Hidden Charges: Some developers add finance charges or service fees that effectively increase your total cost. Calculate the real price you’re paying compared to a traditional mortgage.

Property Completion Risk: Developer financing usually means waiting for construction. Research the developer’s track record and the project’s approval status.

Comparing Your Financing Options

Traditional bank mortgages require down payments but offer certain advantages. Current mortgage rates in Dubai start around 3.99% for the first three years, and you’re buying a property with established legal protections.

Developer payment plans might offer zero down payment but could include higher overall costs when you factor in any charges they add. However, recent initiatives like Dubai’s first-time buyer programme are making property ownership more accessible through flexible payment structures.

Understanding all the costs involved in property purchase helps you make an informed decision. Beyond the down payment, you’ll face DLD registration fees (4% of property value), mortgage fees if applicable, and various administrative costs.

Your Rights as a Buyer

Whether you’re using bank financing or developer payment plans, UAE law protects your interests. The Real Estate Regulatory Agency (RERA) and Dubai Land Department oversee property transactions and ensure developers follow the rules.

If a project faces delays or cancellation, you have legal recourse to recover your payments. Recent changes in banking policies mean buyers now need more upfront cash for certain fees, making it even more important to budget accurately.

Frequently Asked Questions

Can I buy property in Dubai with absolutely no money down?

Yes, through developer payment plans on off-plan properties. However, you’ll still need to pay Dubai Land Department registration fees (4% of property value) upfront. The “zero down payment” refers to no initial payment to the developer.

Is zero down payment the same across all banks?

Banks cannot offer zero down payment mortgages under UAE Central Bank regulations. Any zero down payment offer comes from developers offering their own financing, not traditional bank mortgages.

What’s the minimum down payment for a second home?

UAE nationals need 35% down (65% financing) and expatriates need 40% down (60% financing) for second homes or investment properties, regardless of property value.

Are developer payment plans riskier than bank mortgages?

They carry different risks. Developer plans avoid credit checks but tie you to project completion timelines. Bank mortgages require down payments but offer more regulatory protection and immediate property access on ready properties.

Can I switch from a developer payment plan to a bank mortgage later?

Yes, many buyers do this once the property nears completion. However, you’ll need to meet the bank’s requirements at that time, including having enough equity in the property to satisfy their loan-to-value ratios.

What happens if I miss payments on a developer plan?

Terms vary by developer. Some charge penalties, others may cancel the agreement and retain a portion of payments made. Read your contract carefully and understand the consequences before signing.

Making Your Decision

Zero down payment property offers in the UAE are legal when structured as developer payment plans. They’re not legal through traditional bank mortgages due to Central Bank regulations.

Before committing to any property purchase, whether through bank financing or developer plans:

- Calculate the total cost including all fees and charges

- Verify the developer’s reputation and project approvals

- Understand the payment schedule and your obligations

- Review the contract with a property lawyer

- Compare the total cost against alternative financing methods

The Dubai property market continues to evolve with new financing options, but your due diligence remains the best protection for your investment.

Leave a comment