Young buyers in Dubai often underestimate the upfront cash required to enter the property market. While mortgages cover much of the purchase price, several costs cannot be financed through a loan.

Real estate experts say buyers should have between 25 to 30 per cent of the property value ready in cash. For a Dh1 million property, this means roughly Dh250,000 before you receive the keys.

Key Takeaway

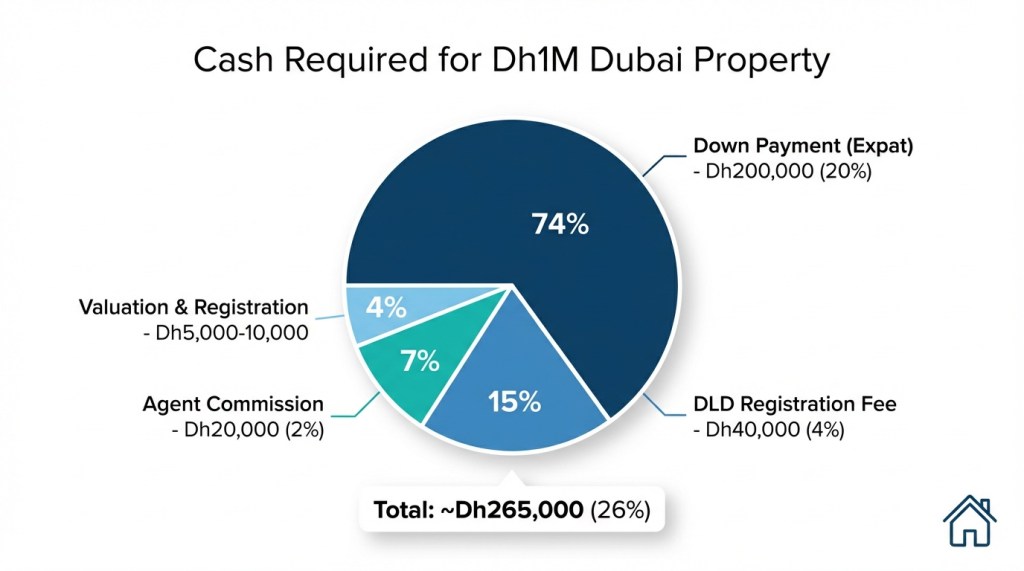

First-time Dubai home buyers need approximately 26% of the property value in cash. This includes a 20% down payment (15% for Emiratis), 4% Dubai Land Department fees, and roughly 2% agent commission. Developers are easing barriers with post-handover plans stretching 20-40% of payments over 2-5 years and booking deposits as low as 5-10%.

What Cash Costs Cannot Be Financed Through a Mortgage?

Several expenses must be paid upfront regardless of your mortgage approval.

Mandatory cash payments:

| Cost | Percentage | Amount (Dh1M Property) |

|---|---|---|

| Down payment (expats) | 20% | Dh200,000 |

| DLD registration fee | 4% | Dh40,000 |

| Agent commission | ~2% | Dh20,000 |

| Valuation and registration | Variable | Dh5,000-10,000 |

| Total | ~26% | ~Dh265,000 |

“The four per cent Dubai Land Department fee and roughly two per cent agency fee must be paid in cash,” said Navneet Mandhani, Founder of Karma Developers.

Even with eased mortgage rates and tenures stretching to 25 years, this initial outlay remains the primary obstacle for first-time buyers.

Understanding the full cost of buying property in Dubai helps avoid financial surprises.

How Much Down Payment Do Expats Need?

The down payment requirement differs based on residency status.

Down payment by buyer category:

| Buyer Type | Minimum Down Payment |

|---|---|

| UAE Nationals | 15% |

| UAE Residents (Expats) | 20% |

| Non-Residents | 25-30% |

For expats purchasing a Dh1.5 million apartment, expect to pay at least Dh300,000 as a down payment before adding registration fees and commissions.

“In most cases, a buyer should have between 25 to 30 per cent of the property value ready in cash,” said Ismail Al Hammadi, Founder & CEO of IAH Group.

The UAE mortgage guide for expats provides detailed bank requirements and approval criteria.

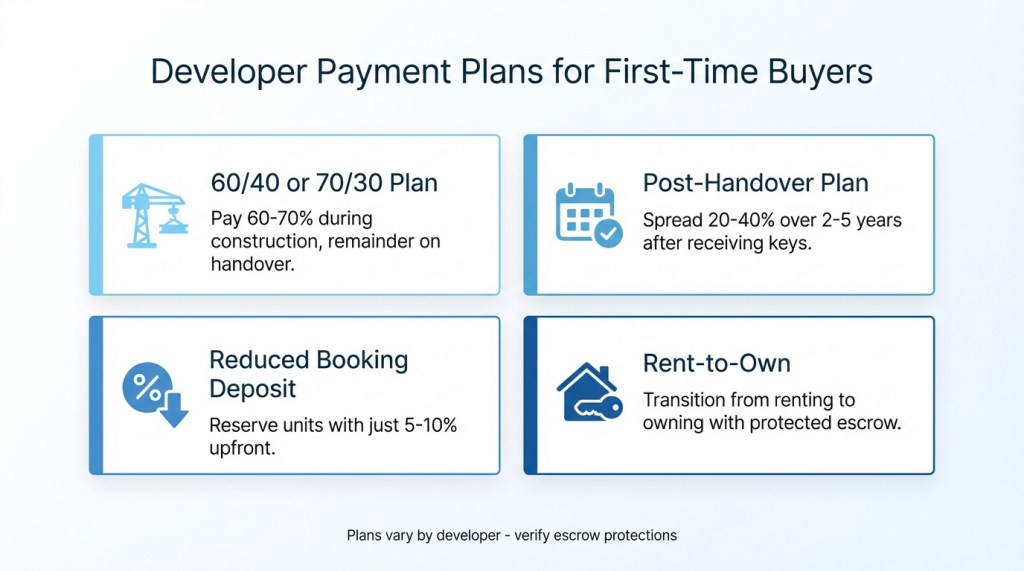

What Payment Plans Are Developers Offering?

To attract younger and first-time buyers, developers have become increasingly creative with payment structures.

Common payment plans available:

- 60/40 or 70/30 during construction: Pay 60-70% during building phase, remainder on handover

- Post-handover plans: Spread 20-40% of payments over 2-5 years after receiving keys

- Reduced booking deposits: As low as 5-10% to reserve a unit

- Rent-to-own options: Depending on developer track record and escrow protections

“Developers have become much more creative with their payment structures. Some are offering post-handover plans that can go up to a 5-year period, while others have reduced upfront payments to as low as 10 per cent,” said Al Hammadi.

This shift explains the surge in young buyers entering the market. First-time buyers are now driving Dubai property growth, with residents purchasing after just 3-5 years in the UAE.

Why Do Young Buyers Face Mortgage Challenges?

Income verification and credit history present hurdles for younger applicants seeking mortgage approval.

Common challenges include:

- Limited credit history in the UAE

- Shorter employment track record

- Income verification requirements

- Debt-to-income ratio assessments

“Young buyers often encounter hurdles when securing mortgages, primarily due to stringent lending criteria related to income verification and credit history,” said Yogesh Bulchandani, CEO & Founder of eSunrise Capital.

However, Bulchandani noted that many are overcoming these challenges through better financial literacy and a more favourable lending environment.

Banks typically require:

- Minimum 6 months employment with current employer

- Salary certificate or bank statements proving income

- Existing debt obligations below certain thresholds

- Clean credit bureau record

The Dubai first-time home buyer incentives programme offers specialised mortgage products through participating banks.

What Help Exists for UAE Nationals?

Emirati citizens benefit from additional support when purchasing property.

Advantages for UAE nationals:

- Lower down payment requirement (15% vs 20%)

- National housing loans and assistance programmes

- Priority access in certain government initiatives

- Special financing schemes through UAE banks

“Young UAE citizens benefit from national housing loans and assistance programmes, which help them access property earlier in life,” noted Bulchandani.

Both citizens and expatriates can access loans from UAE banks with financing options tailored to their status.

How Do Off-Plan vs Ready Properties Compare?

The type of property affects your upfront cash requirements.

Off-plan properties:

- Lower initial deposits (10-20% typically)

- Staged payments during construction

- Post-handover payment options available

- Risk of project delays

Ready properties:

- Full down payment required upfront

- Immediate mortgage arrangement needed

- Move-in within weeks of purchase

- No construction risk

For buyers with limited immediate cash, off-plan properties offer more accessible entry points. The rent or buy decision depends heavily on your financial position and timeline.

What Additional Costs Should Buyers Budget For?

Beyond the purchase transaction, new homeowners face ongoing expenses.

Post-purchase costs:

| Cost | Typical Amount |

|---|---|

| DEWA connection deposit | Dh2,000-4,000 |

| Annual service charges | Varies by community |

| Mortgage arrangement fee | ~1% of loan value |

| Property valuation | Dh2,500-3,500 |

| Mortgage life insurance | 0.4-0.8% annually |

Service charges in Dubai range from Dh3 to Dh30+ per square foot annually depending on the community and facilities provided.

The essential property buying costs guide details all expenses to expect.

Can Property Purchase Lead to Golden Visa?

Property investment can qualify buyers for UAE residency visas.

Visa eligibility through property:

| Property Value | Visa Type |

|---|---|

| Dh750,000+ | 2-year investor visa |

| Dh2 million+ | 10-year Golden Visa |

The Golden Visa through property investment offers long-term residency benefits including family sponsorship and business flexibility.

Recent updates allow Golden Visa eligibility even if the property is mortgaged or off-plan, provided certain payment milestones are met.

What Makes Dubai Property Achievable for Young Buyers?

Despite the upfront costs, experts maintain that property ownership remains financially achievable for young residents.

The key factors include:

- Creative developer payment plans reducing initial barriers

- Eased interest rates making monthly payments competitive

- Government initiatives supporting first-time buyers

- Growing lender appetite for younger applicants

“The initial 26 per cent is the key commitment, making long-term ownership more manageable,” said Mandhani.

Understanding the freehold property ownership process helps buyers prepare for each transaction stage.

Frequently Asked Questions

How much cash do I need for a Dh1 million Dubai property?

Approximately Dh250,000-265,000, covering the 20% down payment, 4% DLD fees, and 2% agent commission plus registration costs.

Can I finance the DLD fees through my mortgage?

No. The 4% Dubai Land Department fee must be paid in cash and cannot be included in mortgage financing.

What is the minimum down payment for expats in Dubai?

Expats must pay a minimum 20% down payment. UAE nationals pay 15%. Non-residents typically pay 25-30%.

Do developers offer payment plans that reduce upfront costs?

Yes. Many developers now offer booking deposits as low as 5-10% and post-handover plans spreading 20-40% of payments over 2-5 years.

What challenges do young buyers face getting mortgages?

Limited credit history, shorter employment records, and stringent income verification requirements can slow approvals. Building credit history and maintaining stable employment helps.

Can I get a visa through buying Dubai property?

Yes. Properties worth Dh750,000+ may qualify for a 2-year investor visa. Properties worth Dh2 million+ may qualify for the 10-year Golden Visa.

What ongoing costs should I budget after buying?

Annual service charges, DEWA connection deposits (Dh2,000-4,000), mortgage life insurance, and community maintenance fees.

How long are mortgage terms in Dubai?

Mortgage tenures can extend up to 25 years, helping reduce monthly payment amounts for borrowers.

Leave a comment