For decades, renting in Dubai meant one thing: hand-writing post-dated cheques. The “1-cheque vs. 4-cheques” negotiation has been a staple of expat life, often forcing tenants to part with massive sums of cash upfront.

However, a major shift is underway. Industry leaders report a growing demand for flexibility, and PropTech platforms are stepping in to bridge the gap. With new partnerships like Property Finder and Keyper, paying rent in 12 digital monthly instalments is becoming a reality for thousands of residents.

But convenience comes at a cost. Here is what you need to know about the new “Rent Now, Pay Later” (RNPL) model.

The Shift to Digital Payments

The momentum for monthly payments is driven by a simple mismatch: tenants get paid monthly, but landlords want their money upfront.

To solve this, platforms like Keyper and Takeem have introduced systems where they pay the landlord the full annual amount in one go, while the tenant pays the platform back in monthly slices.

Cherif Sleiman, Chief Revenue Officer at Property Finder, confirmed that this option will soon be integrated directly into their app.

“Tenants who opt for monthly payments can manage their rent digitally, making it easier to plan their finances… while existing within the general rental framework.”

The Real Cost: Calculating the Premium

While paying monthly sounds ideal, it is not always free. If your landlord originally demanded 1 or 4 cheques, switching to a monthly plan via a third-party platform usually involves a “convenience fee.”

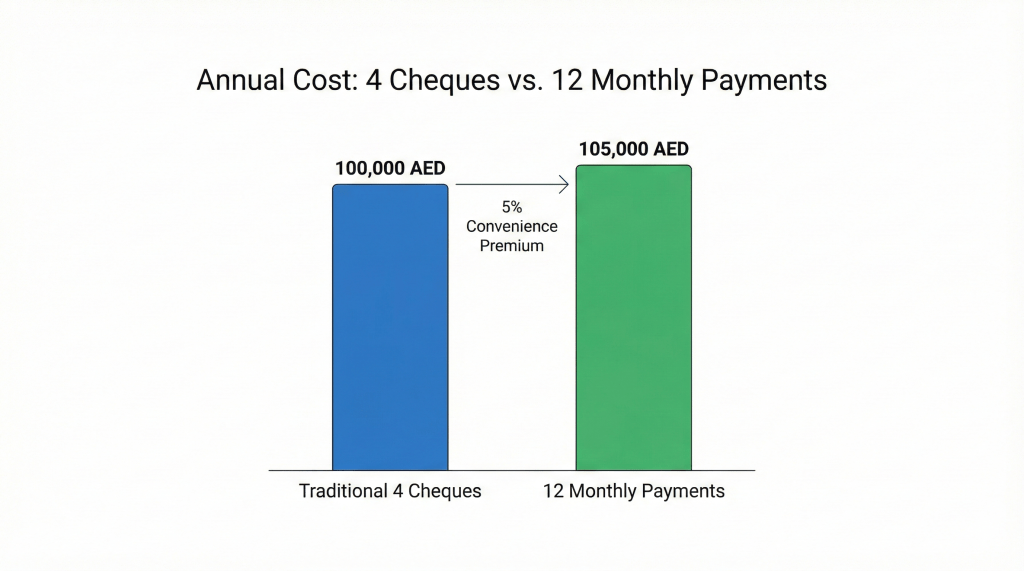

Example Calculation: Let’s say your apartment rent is Dh100,000 per year.

- Traditional (4 Cheques): You pay Dh25,000 every quarter. Total: Dh100,000.

- Monthly (Keyper Model): You pay roughly Dh8,750 per month via credit card.

- Total Annual Cost: Dh8,750 x 12 = Dh105,000.

The Hidden Cost: You are paying a 5% premium (Dh5,000) for the luxury of monthly payments.

How the Model Works

This system essentially functions as a financing product. The platform takes on the risk of the tenant defaulting, which is why they charge the premium.

- Tenant agrees to the monthly price (including the markup).

- Platform pays the Landlord the agreed annual rent upfront (often at a discounted “1-cheque” rate).

- Tenant pays the Platform monthly via direct debit or credit card.

Who Wins?

- Landlords: Get guaranteed cash upfront without chasing cheques.

- Tenants: Get to keep their cash flow smooth and avoid taking out bank loans.

- Platforms: Earn revenue from the markup (the difference between what the tenant pays and what the landlord receives).

Is It Worth It?

Before signing up, compare the 5% platform premium against other financing options.

- Credit Card: Some banks offer 0% instalment plans for rent, but often with a processing fee of 1-2%.

- Personal Loan: Interest rates might be lower than 5% depending on your salary and bank.

However, for many residents, the ease of a digital, paperless experience—and avoiding the hassle of writing 4-12 physical cheques—is worth the extra cost.

Key Takeaway

Monthly rent payments are transforming the Dubai rental market, offering tenants unmatched flexibility. However, this convenience typically comes with a 5% premium. Always calculate the total annual cost before switching from traditional cheques to a digital monthly plan.

Further Reading:

Leave a comment