Your credit score represents one of the most important numbers in your financial life in the UAE. It reflects how reliably you manage debt, pay bills, and meet financial obligations. For just Dh10.50, you can check your credit score through the Etihad Credit Bureau and gain valuable insights into your financial health.

Understanding Your UAE Credit Score

A credit score functions like a financial report card, summarising your past behaviour with loans, credit cards, and various payment obligations. The Etihad Credit Bureau collects information from multiple sources to calculate your score, creating a comprehensive picture of your financial reliability.

Banks, telecom operators, utility companies, and government entities all report your payment behaviour to the bureau. This means that missed or late payments—whether for a personal loan, phone bill, or electricity payment—can negatively affect your score and impact your ability to secure loans or favourable interest rates in the future.

Even small oversights carry consequences. A missed mobile phone bill or late utility payment gets recorded in your credit history, potentially making future financial applications more difficult or expensive.

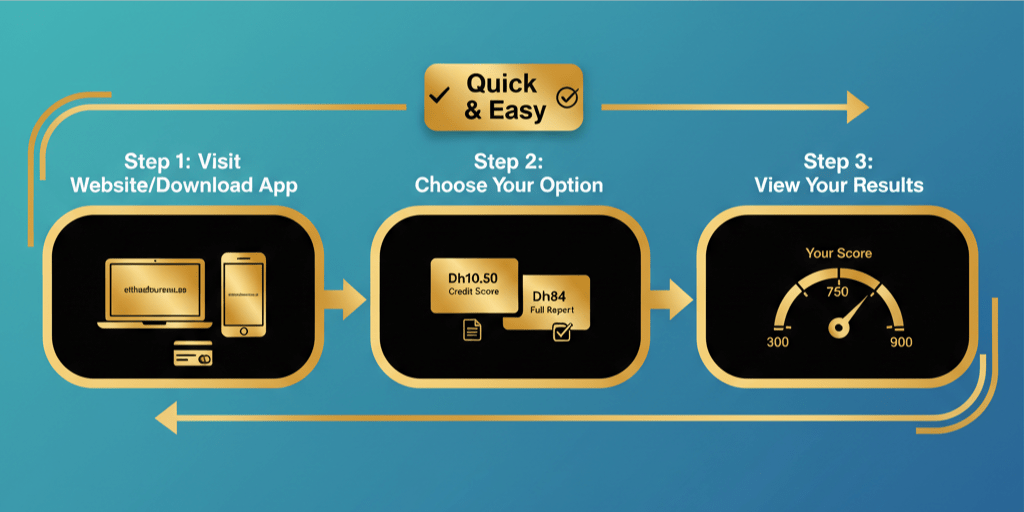

How to Access Your Credit Score

The Etihad Credit Bureau provides two straightforward ways to access your credit information:

Website Access: Visit etihadbureau.ae to purchase your credit score or full report directly through their online portal.

Mobile App: Download the Etihad Bureau application on iOS or Android devices for convenient mobile access to your credit information.

You have two purchase options:

Credit Score Only costs Dh10.50 and provides your numerical credit score, giving you a quick snapshot of your current credit standing.

Full Credit Report costs Dh84 (including VAT) and delivers comprehensive details including your financial obligations, complete repayment history, and your last reported salary. This detailed report shows information drawn from banks, telecom operators, utility companies, and government entities.

The full report provides significantly more context than the score alone, helping you understand exactly what factors influence your credit rating and where you might need to improve.

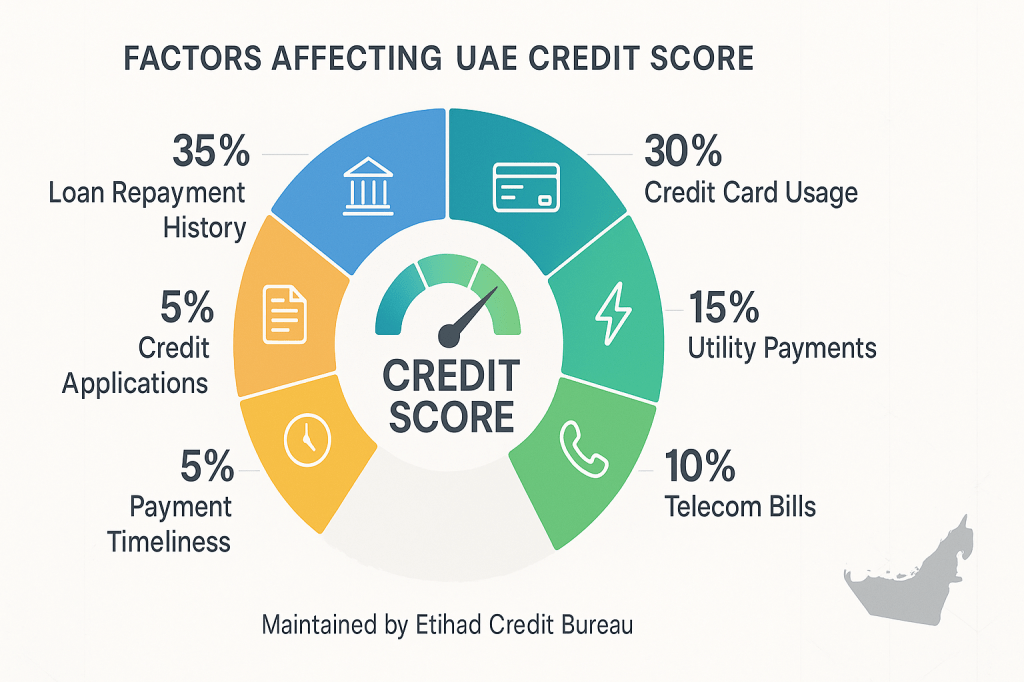

What Influences Your Credit Score

Multiple factors contribute to your credit score calculation:

Loan Repayment History: Your track record of repaying personal loans, car loans, mortgages, and other credit facilities represents the most significant factor. Consistent, timely repayments build strong credit, whilst missed or late payments damage your score substantially.

Credit Card Behaviour: How you manage credit cards affects your score. This includes whether you pay on time, how much of your available credit you use, and whether you frequently max out your cards.

Utility Payments: Regular bills from DEWA, ADDC, SEWA, and other utility providers contribute to your credit history. Late payments or disconnections due to non-payment harm your score.

Telecom Bills: Mobile phone bills from Etisalat and du factor into your credit calculation. Missed payments or disputes that go unpaid appear on your credit report.

Payment Timeliness: The overall pattern of whether you pay obligations on or before due dates influences your score. Consistent late payments signal financial unreliability to lenders.

Credit Applications: Frequent applications for new credit can negatively impact your score, as they may indicate financial stress or desperation for credit.

Understanding these factors helps you make informed decisions about your financial behaviour and identify areas where you can improve your creditworthiness.

Benefits of Maintaining a Good Credit Score

A strong credit score delivers multiple advantages for UAE residents managing their financial lives:

Faster Loan Approvals: Banks and financial institutions process applications more quickly when you demonstrate solid credit history. Good scores indicate lower risk, leading to expedited approval processes.

Lower Interest Rates: Higher credit scores qualify you for reduced interest rates on loans and credit cards. This translates to significant savings over the life of loans, particularly for large obligations like mortgages or car financing.

Higher Credit Limits: Financial institutions offer larger credit amounts to borrowers with proven reliability. Good scores expand your access to credit when you need it.

Greater Financial Confidence: Knowing you maintain good standing with creditors provides peace of mind and confidence in your financial management abilities.

Better Negotiating Position: Strong credit scores give you leverage when negotiating terms on financial products, potentially securing better conditions than standard offerings.

Easier Access to Financial Products: Some premium credit cards, preferential banking services, and specialized financial products require good credit scores for eligibility.

These benefits compound over time, making the difference between expensive, restricted financial access and affordable, flexible options that support your goals.

Why Regular Credit Score Monitoring Matters

Checking your credit score isn’t a one-time activity. Regular monitoring provides several important benefits:

Early Problem Detection: Identifying score drops quickly allows you to investigate and address issues before they worsen. You might discover missed payments you weren’t aware of or billing errors affecting your score.

Error Identification: Credit reports occasionally contain mistakes—accounts that aren’t yours, payments marked late when they weren’t, or outdated information that should have been removed. Regular checks help you catch and dispute these errors.

Identity Theft Protection: Unexpected changes in your credit report could indicate fraudulent activity. Regular monitoring helps you detect unauthorized credit applications or suspicious activity quickly.

Loan Application Preparation: If you’re planning to apply for a mortgage, car loan, or other major credit, checking your score beforehand shows you what lenders will see. This allows time for improvement if needed.

Progress Tracking: If you’re actively working to improve your credit score, regular checks help you measure progress and confirm that positive changes reflect in your score.

Financial Planning: Understanding your credit position helps with broader financial planning, particularly for major life decisions involving credit.

How to Improve Your Credit Score

If your credit score needs improvement, several strategies can help:

Pay All Bills on Time: Set up automatic payments or reminders for due dates. Even small bills matter—telecom and utility payments count toward your credit history.

Reduce Credit Card Balances: Aim to use less than 30% of your available credit limit. High utilization rates signal financial stress to lenders.

Maintain Older Credit Accounts: Length of credit history contributes to your score. Keep older accounts active even if you don’t use them frequently.

Limit New Credit Applications: Apply for new credit only when necessary. Multiple applications in short periods can lower your score.

Address Outstanding Debts: Focus on clearing any overdue balances. Contact creditors about payment plans if you’re struggling with obligations.

Dispute Errors Promptly: If you find mistakes in your credit report, file disputes with Etihad Credit Bureau immediately with supporting documentation.

Diversify Credit Types: A mix of credit types (installment loans, credit cards, etc.) can positively influence your score, though this should happen naturally rather than forcing applications.

Improvement takes time—typically several months of consistent positive behaviour before significant score increases appear. Patience and discipline are essential.

Understanding Credit Score Ranges

UAE credit scores typically range from 300 to 900, with different ranges indicating varying levels of creditworthiness:

Excellent (750-900): Strong credit management with minimal risk. Qualifies for best interest rates and terms.

Good (700-749): Solid credit behaviour with few concerns. Eligible for most financial products with favourable terms.

Fair (650-699): Average credit management with some concerns. May face higher interest rates or stricter conditions.

Poor (600-649): Significant credit issues present. Limited access to credit with unfavourable terms.

Very Poor (300-599): Serious credit problems. High likelihood of loan rejections or extremely restrictive terms.

Knowing where you fall within these ranges helps set realistic expectations for loan applications and financial product access.

For New UAE Residents

If you’ve recently arrived in the UAE, you won’t have a credit score initially. This doesn’t mean you have bad credit—you simply haven’t established credit history yet.

Building credit from scratch requires:

Opening a Bank Account: Establishing banking relationships forms the foundation of your financial presence.

Obtaining a Credit Card: Even a basic credit card with a low limit helps build history. Use it sparingly and pay in full each month.

Setting Up Utility Accounts: Registering utilities in your name and paying consistently establishes positive payment history.

Paying Bills Punctually: Every on-time payment contributes to building your credit profile.

Avoiding Early Mistakes: Be particularly careful during your first months, as negative marks impact a thin credit file more severely than an established one.

New residents should check their credit report after six to twelve months to confirm accurate reporting and begin tracking their credit development.

When to Check Your Credit Score

Consider checking your credit score in these situations:

Before Major Purchases: Planning to buy a car or property? Check your score several months in advance to address any issues.

Before Loan Applications: Know what lenders will see before submitting applications. This prevents surprises and allows time for improvement.

After Clearing Debts: Verify that paid-off loans and settled accounts reflect correctly in your credit report.

Annually as Routine: Even without immediate credit needs, annual checks help maintain awareness of your financial standing.

After Billing Disputes: Following resolution of any payment disputes, confirm that your credit report reflects the outcome correctly.

When Changing Jobs: Salary changes and employment status updates eventually appear in credit reports. Verify accuracy after job transitions.

The Dh10.50 cost for a credit score check represents minimal investment compared to the insights gained and potential problems prevented.

Taking Control of Your Financial Future

Your credit score isn’t merely a number—it’s a gateway to financial opportunities and freedom. Managing it actively rather than ignoring it puts you in control of your financial destiny in the UAE.

Regular monitoring, responsible credit behaviour, and prompt attention to issues create a virtuous cycle. Good credit opens doors to better financial products, which—when managed well—further strengthen your credit, expanding your options continuously.

For the cost of a meal or coffee, checking your credit score provides valuable information that can save you thousands of dirhams in interest payments and prevent costly rejections at critical moments.

Make credit score monitoring part of your regular financial routine. Your future self will thank you when you need credit and find yourself in an excellent position to secure it on favourable terms.

Frequently Asked Questions

How much does it cost to check credit score in UAE?

You can check your credit score for Dh10.50 through the Etihad Credit Bureau website or mobile app. A full credit report costs Dh84 including VAT.

How do I check my Etihad Credit Bureau score?

Visit etihadbureau.ae or download the Etihad Bureau app on iOS or Android. Purchase either the credit score (Dh10.50) or full report (Dh84) through the platform.

What is considered a good credit score in UAE?

Credit scores above 700 are generally considered good in the UAE. Scores above 750 are excellent, whilst scores below 600 may result in loan rejections or unfavourable terms.

What affects my UAE credit score?

Loan repayment history, credit card payment behaviour, utility bill payments, telecom bill payments, payment timeliness, and frequency of credit applications all affect your UAE credit score.

Can utility bills affect my credit score?

Yes, utility bills from DEWA, ADDC, SEWA and other providers are reported to Etihad Credit Bureau. Late payments or disconnections due to non-payment can negatively impact your score.

How long does it take to improve credit score in UAE?

Improving credit scores typically takes several months of consistent positive behaviour. Significant improvements usually become visible after 3-6 months of on-time payments and responsible credit management.

Do telecom bills affect credit score?

Yes, mobile phone bills from Etisalat and du are reported to Etihad Credit Bureau. Missed payments or unpaid bills can harm your credit score.

Can I dispute errors on my UAE credit report?

Yes, if you find incorrect information in your credit report, you can file a dispute with Etihad Credit Bureau with supporting documentation to have errors corrected.

What is included in the full credit report?

The full credit report (Dh84) includes your financial obligations, complete repayment history, last reported salary, and detailed information from banks, telecom operators, utilities, and government entities.

How often should I check my credit score?

Check your credit score at least annually as routine maintenance, and additionally before major loan applications, after clearing debts, or when planning significant financial decisions.

Further Reading

For more information about managing finances and living in the UAE:

- The Complete Cost to Live in Dubai as an Expat in 2025

- Work in the United Arab Emirates: Complete Guide 2025

- Jobs in Dubai for Foreigners: Your 2025 Guide

- UAE Golden Visa Guide 2024: Dh30,000 Salary Requirements

- Your Essential Checklist for Moving to the UAE in 2025

Stay updated with essential UAE living and financial information by following JobXDubai.

Leave a comment