By JobXDubai Team | November 20, 2025

In a massive shift for the country’s financial sector, the UAE has officially removed the long-standing Dh5,000 minimum salary requirement for personal loan approvals.

For years, this rule defined who could access credit and who was left out. Now, the Central Bank has handed the decision-making power back to individual banks. This move opens the door for millions of residents—particularly low-income workers, part-time staff, and those starting their careers—to enter the formal banking system.

However, while access has widened, experts warn that new freedoms come with new responsibilities. Here is what you need to know before you sign on the dotted line.

The End of the Dh5,000 Floor

Previously, if your salary was under Dh5,000, getting a legal personal loan from a major bank was nearly impossible. Banks are now expected to introduce micro-loans and credit products specifically designed for this newly eligible segment.

Faizan Mandavia, Group CEO of FAM Group, notes that while more people are eligible, the costs may vary.

“Banks are likely to offer micro-loans or entry-level credit products to tap into this newly opened segment.” — Faizan Mandavia, CEO of FAM Group

This shift aims to move workers away from informal, unregulated lenders and into a safer, structured banking environment. For context on salary structures in the region, read our Minimum Wage in UAE: Complete Guide for 2025.

The New Rules: Caps and Limits

It is important to understand that “no minimum salary” does not mean “unlimited borrowing.” strict regulatory guardrails remain in place to protect you from over-leveraging.

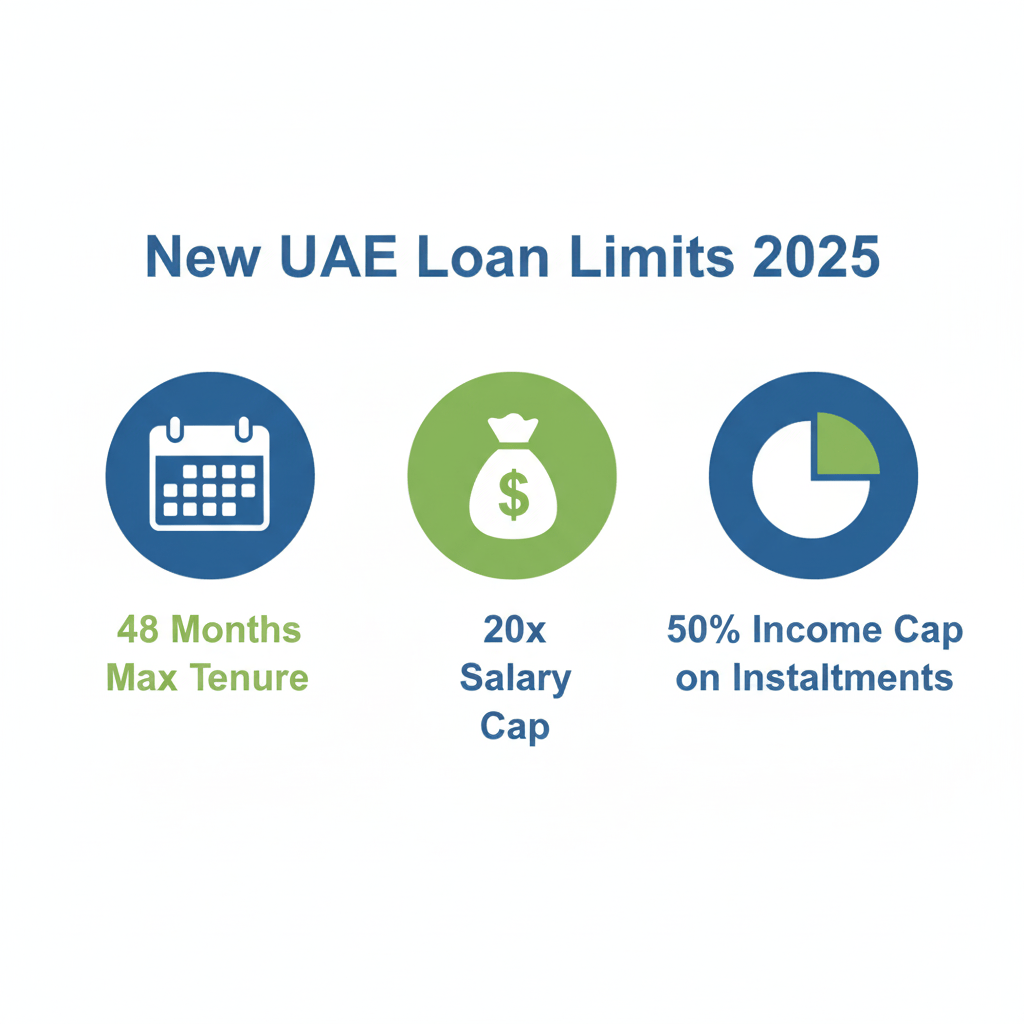

Regardless of your income, the following limits apply:

- Loan Amount: Cannot exceed 20 times your monthly salary.

- Instalment Limit: Monthly repayments cannot exceed 50% of your gross income.

- Repayment Term: The maximum tenure for a personal loan is 48 months (4 years).

The Hidden Costs: Interest and Risk

Just because you can borrow, doesn’t always mean you should.

Vijay Valecha, Chief Investment Officer at Century Financial, warns that lenders will need to manage the higher risk associated with lower-income loans. Consequently, applicants in lower salary brackets should expect higher interest rates or stricter verification processes compared to high-income earners.

Mandavia advises residents to look beyond the advertised rate. You must check the effective interest rate, processing fees, and total repayment amount. Understanding the full cost of the loan is vital to avoid financial strain.

The Role of WPS (Wage Protection System)

The new system relies heavily on the Wage Protection System (WPS). Banks are comfortable lending to lower-income segments because repayments are often automated through salary deductions. This system ensures that loan repayments are prioritized before the salary reaches your pocket. To understand how these deductions work legally, check our guide on UAE Salary Deduction Rules: Legal Guidelines for Private Companies 2025.

What happens if you lose your job?

This is a critical risk. If your salary stops, the automatic deductions stop.

- Immediate Action: You must contact your bank the moment your employment status changes.

- Restructuring: Job loss does not automatically pause your loan. You must formally request a payment holiday or restructuring plan.

- New Job: You will need to coordinate with your new employer to route your salary correctly to satisfy the bank’s requirements.

Moving Away from Informal Lenders

This policy is a lifeline for many. It allows workers to build a credit history through the Al Etihad Credit Bureau (AECB), which was previously impossible for those earning under Dh5,000.

By providing access to regulated Buy Now, Pay Later (BNPL) options and WPS-linked overdrafts, the market effectively reduces the reliance on predatory, informal lending circles that often trap workers in debt.

However, you must remain cautious. Valecha highlights early warning signs of debt stress:

- Monthly repayments hitting 50% of your income.

- Using cash advances to pay off other debts.

- Relying on short-term credit rollovers.

FAQ: New Loan Rules

1. Can I get a loan if I earn Dh3,000?

Yes, technically. Banks can now approve loans for salaries under Dh5,000. However, approval depends on the specific bank’s risk appetite and your credit score.

2. Will the interest rate be higher?

Likely, yes. Lower-income loans are considered higher risk, so banks may charge higher rates to offset this.

3. How much can I borrow?

You are capped at 20 times your monthly salary. If you earn Dh4,000, the absolute maximum loan amount would be Dh80,000, provided your monthly instalments don’t exceed Dh2,000 (50% of salary).

4. Do I need a credit score?

Yes. Banks will look closely at your Al Etihad Credit Bureau score and the reputation of your employer to assess your application.

Key Takeaway

The removal of the minimum salary requirement allows millions of UAE residents to access safer, legal credit options. However, borrowers must be vigilant about interest rates and strictly adhere to the rule that debt repayments should never exceed half of their monthly income.

Further Reading:

Leave a comment