Key Takeaway: Federal Decree Law No. (6) of 2025 grants UAE Central Bank unprecedented authority with fines up to Dh1 billion, power to directly withdraw penalties from violator accounts, early intervention rights in failing institutions, and expanded oversight of banks, insurers, fintech firms, and payment providers through the unified Sanadak platform.

The UAE financial sector faces its biggest regulatory transformation in years. A sweeping new law dramatically increases penalties for violations and gives the Central Bank powers to act before institutions collapse.

What Changed Under the New Financial Law?

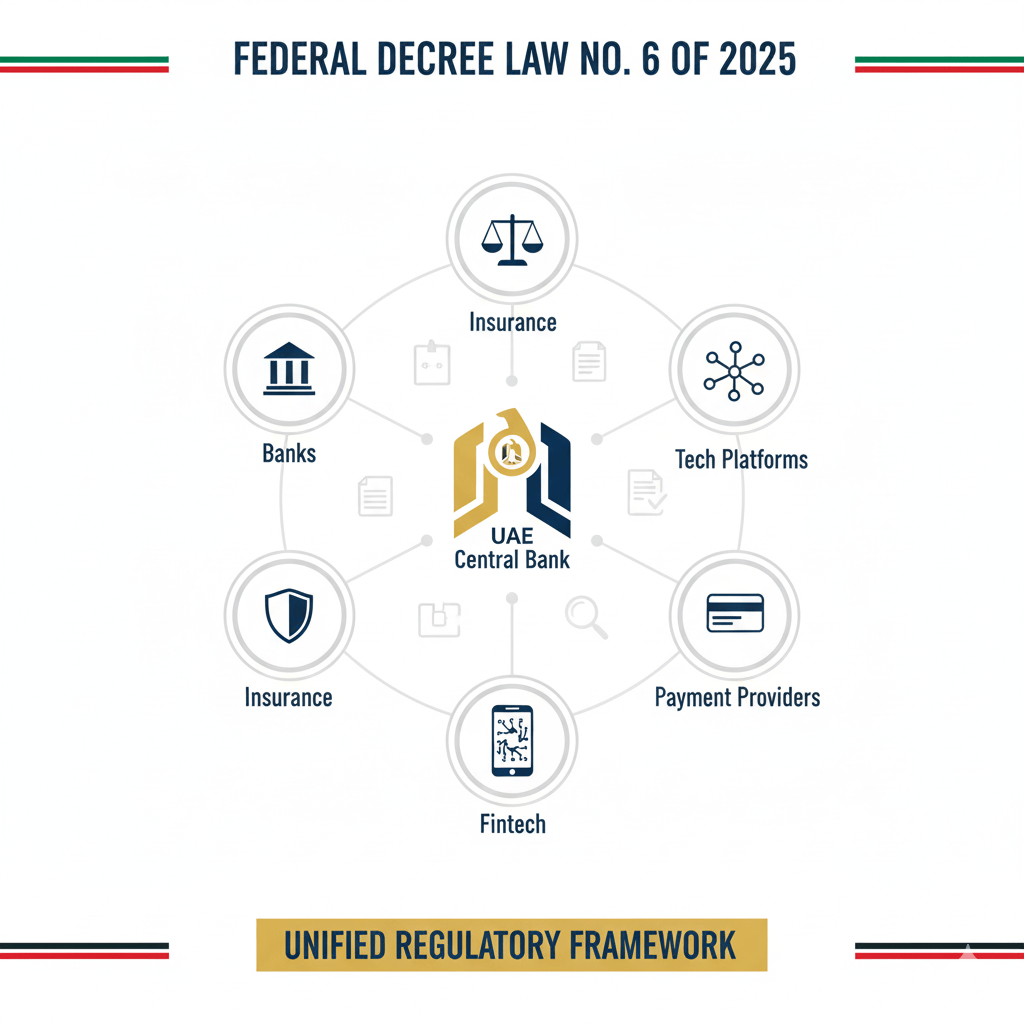

Federal Decree Law No. (6) of 2025 reshapes how the UAE Central Bank supervises financial institutions. The law covers banks, insurance companies, fintech enterprises, tech platforms, payment system providers, and other financial service players.

Ali Dakhlallah, Senior Associate at Habib Al Mulla & Partners, explains the shift: “This law gives the regulator the authority to act pre-emptively, decisively and directly.”

The changes affect every licensed financial entity in the UAE. Banks and insurers now face stronger scrutiny, with regulators able to step in earlier and more forcefully when problems emerge.

Similar regulatory enforcement in the banking sector has already demonstrated the Central Bank’s commitment to maintaining system integrity.

How High Are the New Fines?

Administrative fines have increased dramatically. Penalties can reach up to 10 times the value of violations in some cases.

The law sets a maximum fine ceiling of Dh1 billion. This massive threshold gives regulators substantial enforcement power against banking and insurance institutions.

Minimum fines apply for specific violations. Unlicensed activity or promotional work requiring licences but conducted without proper authorisation face mandatory penalties.

The legal expert noted: “The Dh1-billion fine threshold gives the Central Bank long and sharp nails to enforce against banking and insurance institutions. This high threshold also incentivises more strict compliance processes to prevent money laundering and financial crime violations.”

Can the Central Bank Take Money Directly From Accounts?

Yes. The Central Bank may now withdraw penalties directly from accounts held by violators before a final judicial ruling.

This power represents a significant shift from previous enforcement procedures. Financial institutions can no longer delay penalty payments through lengthy legal processes.

The regulator can also publish penalties and settlement decisions online. This transparency measure aims to enhance market discipline and public accountability.

Understanding consumer financial protection rights becomes increasingly important as regulatory oversight intensifies.

What Are Early Intervention Powers?

The Central Bank can now act much sooner when institutions show distress signals. Regulators no longer need to wait for critical failures before taking action.

The regulator can compel corrective action in multiple ways:

Impose liquidity or capital requirements on struggling institutions. Replace board members or senior management showing poor performance. Transfer assets to protect customer interests. Take direct control of the institution if necessary.

Dakhlallah added that the regulator is authorised “to directly step into the shoes of the institution’s senior management.”

This proactive approach aims to prevent small problems from becoming systemic crises.

How Does the Resolution Authority Work?

The decree confirms the Central Bank’s role as the national Resolution Authority with powers to manage crisis situations.

During financial emergencies, the Central Bank can:

Remove and appoint management teams. Recover funds from responsible individuals. Restructure capital to restore stability. Transfer or sell assets to preserve critical functions.

The law enables the Central Bank to establish temporary entities for essential service continuity. If recovery proves impossible, regulators can carry out organised liquidation.

These powers mirror international best practices seen in major financial centres worldwide.

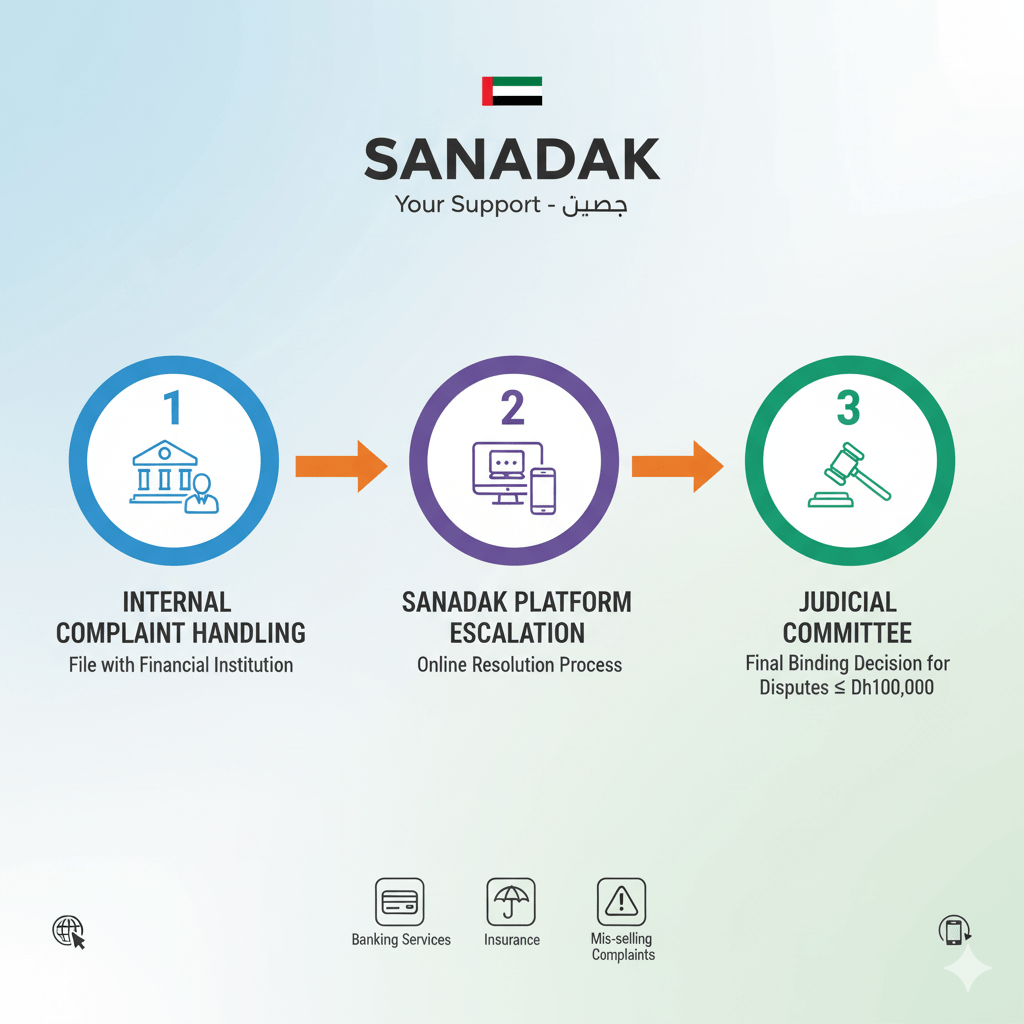

What Is the Sanadak Platform?

The law strengthens consumer protection by consolidating financial complaints under the Sanadak platform.

Dakhlallah describes it as “one of the most people-facing changes in the new law and is designed to make the financial system feel simpler, fairer, and more accessible to average consumers.”

The Central Bank launched Sanadak (Arabic for “Your Support”) in 2023 for banking complaints. Under the new law, Sanadak becomes the unified dispute-resolution platform for both banks and insurance complaints.

Customers can file complaints online or via mobile apps covering:

Banking services including loans, credit cards, payments, and fees. Insurance claims and coverage disputes. Mis-selling, delays, or non-responsiveness by financial institutions.

The three-stage dispute resolution process begins with internal complaint handling, followed by escalation to Sanadak and finally a specialised judicial committee.

For disputes up to Dh100,000, the committee’s ruling becomes final and enforceable. This provides faster resolution than traditional court proceedings.

The change creates “one law, one regulator, one complaint platform (Sanadak) and enforceable resolutions.”

Similar consumer protection frameworks exist for product recalls and filing complaints across other sectors.

Does the Law Address Environmental Concerns?

Yes. The Central Bank now has a statutory mandate to integrate ESG (environmental, social, and governance) principles into its activities and operations.

Dakhlallah highlighted the regulator’s expanded role, noting “a sustainable finance mandate, as its principle objectives now include integrating environmental, social and governance principles into the Central Bank’s activities and operations.”

This aligns the UAE with global sustainability trends and international financial standards.

The ESG mandate affects how banks evaluate lending decisions, investment strategies, and risk assessment frameworks.

How Long Do Financial Institutions Have to Comply?

Financial institutions and market participants have one year to comply with new requirements. Extensions may be granted in specific circumstances.

Unlicensed entities must determine whether they now fall under Central Bank licensing rules.

Banks need to strengthen:

Anti-money laundering (AML) screening procedures. Know Your Customer (KYC) processes. Reporting systems and documentation.

Virtual asset service providers must align with the new supervisory structure. Islamic finance institutions require oversight by the Higher Sharia Authority under the new framework.

The transformation impacts AI banking operations and financial technology platforms already operating in the market.

Frequently Asked Questions

Who does the new financial law affect?

The law regulates banks, insurance companies, fintech enterprises, tech platforms, payment system providers, and other financial service players operating in the UAE.

Can fines really reach Dh1 billion?

Yes. The law establishes Dh1 billion as the maximum administrative fine ceiling. Actual fines depend on violation severity and detailed schedules for specific infractions.

What happens if my bank fails under the new law?

The Central Bank can intervene earlier to prevent failures. If a bank does fail, the Resolution Authority can transfer your deposits to another institution, ensuring continuous access to your money.

How do I use the Sanadak platform?

Visit the Sanadak website or download the mobile app. File complaints online covering banking or insurance issues. The platform provides three-stage resolution including internal handling, Sanadak escalation, and judicial committee review.

Does this affect credit card fraud protection?

Yes. The strengthened regulatory framework enhances consumer protection for banking fraud, though specific fraud protection rules remain under separate regulations.

Will this make banking more expensive?

Financial institutions may pass some compliance costs to customers through fees. However, stronger regulation typically improves system stability, protecting customer deposits and reducing systemic risks.

What should fintech companies do now?

Review whether your operations require Central Bank licensing. Implement strong AML and KYC processes. Prepare documentation for regulatory approval within the one-year compliance period.

How does this compare to international standards?

The UAE’s framework aligns with Basel Committee standards and international best practices. The early intervention and resolution powers mirror systems in major financial centres like London, New York, and Singapore.

Further Reading

- UAE Central Bank Fines Bank Dh5 Million for AML Violations

- UAE Bank Fraud Compensation: When Banks Must Refund Scam Victims

- AI Banking Revolution in UAE: Job Market Shifts & Digital Transformation 2025

- AE Coin: UAE Central Bank Approves First Dirham-Backed Stablecoin

- Financial Services Salaries in Dubai/UAE for 2024

Leave a comment