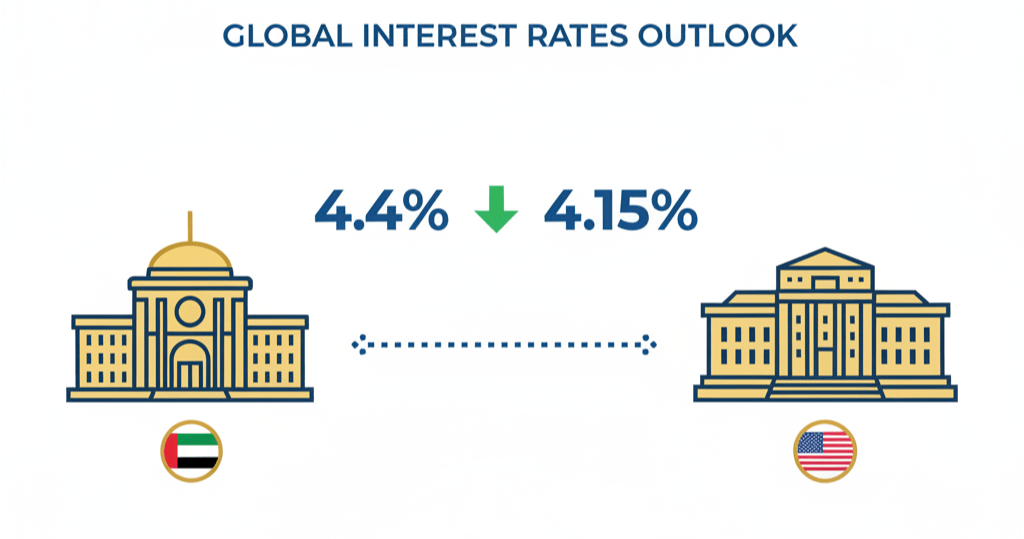

The UAE Central Bank has slashed interest rates to 4.15% from 4.4%, following the US Federal Reserve’s decision to cut rates by 25 basis points. This monetary policy shift promises to reshape the financial landscape for residents and businesses across the Emirates.

Why Did Rates Fall?

The Federal Reserve’s rate reduction prompted the UAE’s move, as the dirham remains pegged to the US dollar. America’s central bank cited a cooling labour market and mounting economic pressures as key factors behind their 25-basis-point cut, bringing the federal funds rate to 4.00%-4.25%.

This marks the first significant policy shift of 2025, with the Fed responding to slower job growth and persistently elevated inflation concerns.

Winners and Losers: Who Benefits Most?

Property Market Gains Momentum

Dubai’s real estate sector stands to benefit considerably from reduced mortgage rates. Homebuyers can expect more attractive financing options, whilst property developers may secure project funding at improved terms.

“Those who wish to invest in property could benefit from a dip in mortgage rates. Even property developers can secure funding at more favourable rates, which could help expedite the launch of projects,” explains Vijay Valecha, Chief Investment Officer at Century Financial.

Business Investment Gets a Boost

Small and medium enterprises (SMEs) alongside large corporations can now access credit at more competitive rates. This financial relief may accelerate business expansion plans and encourage new ventures across various sectors.

The tourism, retail, and hospitality industries particularly stand to gain as cheaper credit facilitates growth initiatives and infrastructure development.

Stock Markets vs Fixed Deposits

Traditional savers face a challenging environment as fixed deposit returns decline. However, equity markets typically respond positively to rate cuts, especially growth stocks and dividend-paying companies.

“While rate cuts typically erode returns from traditional investments, such as fixed deposits, they can translate into gains for the stock market,” notes Valecha.

Regional Impact: Gulf States Feel the Effect

The rate reduction extends beyond the UAE, with neighbouring Gulf countries experiencing similar economic effects. Jordan may see particularly pronounced benefits, according to Hamza Dweik, Head of Trading MENA at Saxo Bank.

“For households struggling under heavy debt obligations, lower interest rates could meaningfully ease financial pressure,” Dweik explains.

What This Means for Your Career

Lower borrowing costs often stimulate economic activity, potentially creating new job opportunities across multiple sectors:

- Construction and Real Estate: Increased property development projects

- Retail and Hospitality: Enhanced consumer spending power

- Financial Services: Growing demand for lending products

- Manufacturing: Improved export competitiveness due to currency effects

Banking Sector Adjustments

Banks face narrower profit margins but anticipate increased lending activity to offset this impact. The shift toward higher-quality assets as repayment risks decrease also supports long-term profitability.

Investment Strategy Shifts

Financial advisors recommend investors reconsider their portfolios, moving away from fixed-income instruments toward equities, real estate, and alternative investments that perform better in low-rate environments.

Looking Forward

The timing proves advantageous for the UAE’s economic diversification goals. Infrastructure projects, business expansion, and foreign direct investment may all receive a significant boost from these improved financing conditions.

A weaker dollar could further support UAE exports, making non-oil goods more competitive internationally whilst potentially supporting crude oil prices.

FAQ Section

Q: How quickly will mortgage rates change? A: Most banks adjust their rates within 1-2 weeks of Central Bank announcements, though the exact timing varies by institution.

Q: Should I refinance my existing mortgage? A: Consider refinancing if your current rate exceeds the new market rates by more than 0.5%. Consult your bank about refinancing options and associated costs.

Q: Will savings account returns decrease immediately? A: Yes, savings and fixed deposit rates typically adjust within a month of Central Bank rate changes.

Q: How does this affect business loan applications? A: Lower rates make business expansion more affordable. Banks may also relax lending criteria slightly, improving approval chances for qualified applicants.

Q: Will credit card rates fall too? A: Credit card rates may decrease, but typically less than mortgage or business loan rates due to higher associated risks.

Leave a comment