Can you own a car in the UAE without traditional financing hassles? Yes, rent-to-own schemes now offer an alternative path to vehicle ownership, eliminating down payments and bank loan requirements whilst providing fixed monthly payments that cover insurance, maintenance, and registration.

For UAE residents, particularly new expatriates, freelancers, and young professionals, traditional car financing presents significant barriers. Bank requirements have become increasingly stringent, with higher salary thresholds and substantial down payments often reaching 20% of the vehicle’s value. This is where rent-to-own programmes are changing the automotive landscape.

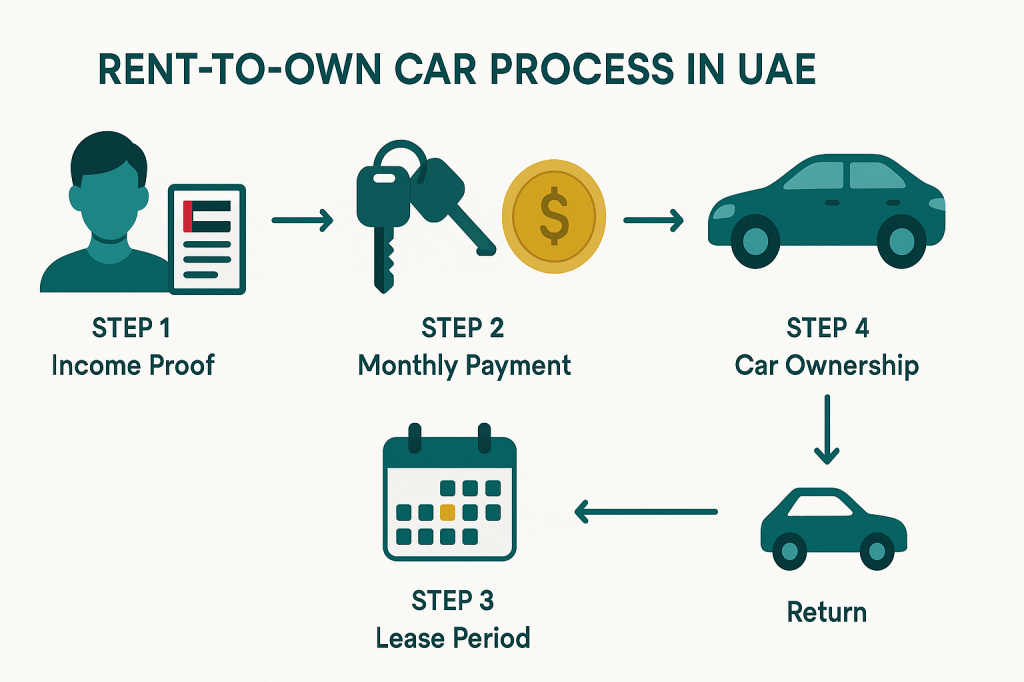

What Are Rent-to-Own Car Schemes in the UAE?

Rent-to-own programmes bridge the gap between rental and ownership. Unlike short-term car rentals with no ownership option, these schemes allow customers to eventually own the vehicle after completing a fixed lease period. The key difference from traditional financing is the absence of upfront costs.

Rahul Singh, Managing Director of Thrifty Car Rental, explains the appeal: “A customer who has recently moved to the UAE and needs a reliable car for daily use might find traditional financing challenging due to down payments, lengthy loan terms, and fluctuating interest rates.”

Traditional bank loans typically require:

- 20% down payment

- 3-5% annual interest rates

- Processing fees

- Finance charges

- Lengthy approval processes

Rent-to-own schemes eliminate all these barriers.

How Do Rent-to-Own Car Programmes Work?

The process is straightforward. Customers pay a fixed monthly fee covering all vehicle-related expenses including insurance, maintenance, and registration. At the lease conclusion, they can purchase the car at a predetermined price or return it without penalties.

Marwan Almulla, General Manager of Dollar Car Rental, outlines their approach: “Dollar’s rent-to-own model allows customers to lease a vehicle for terms ranging from 12 to 60 months. The lease includes an annual mileage allowance of up to 30,000km, with flexibility to increase if needed.”

Key Features Include:

No Initial Costs: Zero down payment, interest, or processing fees All-Inclusive Payments: Monthly fee covers insurance, registration, and maintenance Flexible Terms: Lease periods from 12 to 60 months Mileage Allowances: Up to 30,000km annually with expansion options Purchase Option: Pre-agreed buyout price at lease end

What Determines the Final Purchase Price?

A crucial aspect of rent-to-own schemes is the upfront agreement on the vehicle’s buyout price. This figure is calculated based on expected depreciation, lease term, and other market factors.

“The final purchase amount is decided right at the start of the lease, in consultation with the customer. This means everything is clear from day one, with no surprises down the line,” says Almulla.

This transparency provides significant advantages:

- Price Protection: Locked-in rates regardless of market fluctuations

- Budget Certainty: No unexpected costs at lease end

- Market Independence: Purchase price unaffected by depreciation

The buyout amount isn’t included in monthly instalments but paid as a one-time lump sum if the customer chooses ownership.

Who Is Eligible for Rent-to-Own Car Schemes?

These programmes target both UAE citizens and expatriates. Eligibility requirements are notably more flexible than traditional bank financing.

Primary Requirements:

- Valid proof of income

- Basic risk assessment

- Credit check through Al Etihad Credit Bureau

Singh emphasises inclusivity: “We aim to keep the model as accessible as possible, but verifying income helps us assess affordability and prevents customers from overextending themselves.”

The companies conduct credit checks for risk management whilst maintaining more flexibility than traditional lenders.

What Happens After the Lease Period?

Once customers purchase their vehicle, they assume full responsibility for all ongoing costs. The comprehensive service bundle ends with ownership transfer.

“All services that were bundled with the lease will no longer be available as part of the offering,” notes Singh.

However, companies recognise customer needs for continued support. Almulla adds: “For those who’d like to continue with the convenience they’ve gotten used to, we do offer extended service packages that can be purchased separately.”

Post-ownership responsibilities include:

- Maintenance costs

- Insurance renewals

- Repair expenses

- Registration renewals

How Much Can You Save with Rent-to-Own?

Industry data suggests significant savings potential. Customers using Thrifty’s lease-to-own service report annual savings of 5-15% compared to traditional financing.

These savings result from:

- No Interest Charges: Unlike bank loans with 3-5% annual rates

- Bundled Services: Competitive rates for insurance and maintenance

- No Processing Fees: Elimination of bank charges and administration costs

With rising interest rates and tighter lending requirements, the cost advantage becomes increasingly attractive.

What’s Driving the Growth of Rent-to-Own?

Market projections indicate substantial growth ahead. Dollar has allocated 25% of its fleet to rent-to-own offerings, with plans for expansion as awareness increases.

Almulla predicts: “We expect around 20% of customers who currently go through traditional bank financing will switch to rent-to-own over the next two to four years.”

Market Drivers Include:

- Rising interest rates making traditional loans expensive

- Inflation affecting purchasing power

- Tighter bank lending requirements

- Growing demand from first-time buyers and self-employed individuals

Frequently Asked Questions

How long are rent-to-own lease terms?

Lease terms typically range from 12 to 60 months, providing flexibility to match different budgets and preferences.

What happens if I exceed the mileage allowance?

Most programmes include up to 30,000km annually, with options to increase limits or pay additional fees for excess mileage.

Can I return the car without buying it?

Yes, customers can return vehicles at lease end without penalties or obligation to purchase.

Are there any hidden costs in rent-to-own schemes?

Reputable programmes are transparent about all costs, with the purchase price agreed upfront and monthly payments covering all services.

How does credit history affect rent-to-own eligibility?

Whilst companies conduct credit checks, requirements are typically more flexible than traditional bank loans, focusing on income verification and basic risk assessment.

Key Takeaway

Rent-to-own car schemes in the UAE provide a viable alternative to traditional financing, particularly benefiting new residents, freelancers, and those seeking flexible vehicle ownership paths. With transparent pricing, comprehensive service bundles, and no upfront costs, these programmes are reshaping how people approach car ownership in the Emirates.

Leave a comment