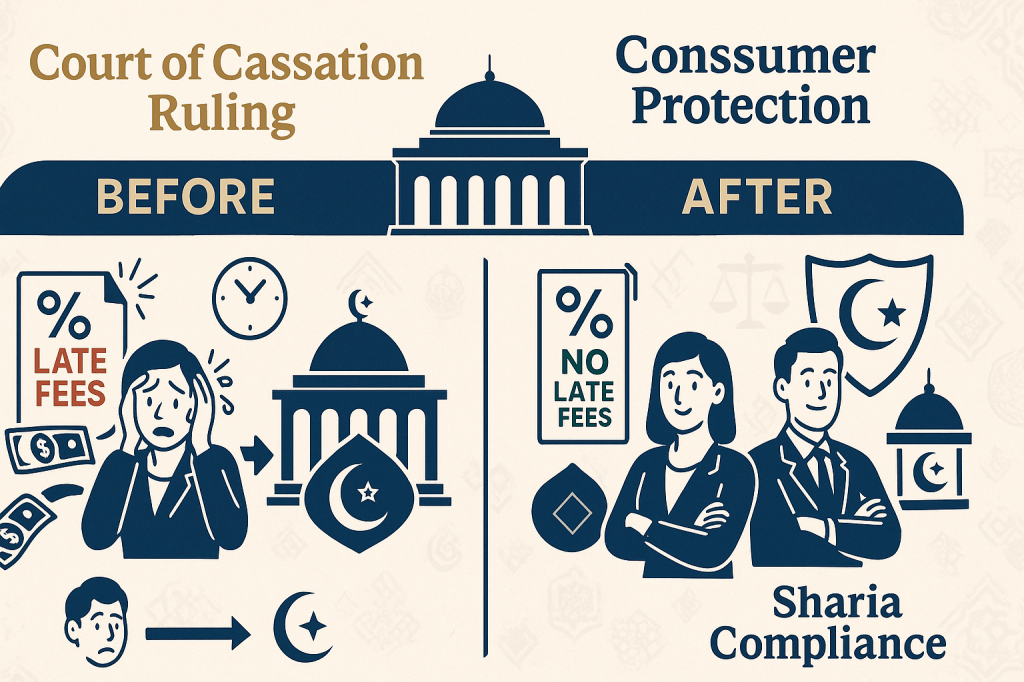

Dubai’s Court of Cassation has issued a groundbreaking ruling that prohibits Islamic banks and Takaful companies from charging late payment fees or interest on delayed obligations, regardless of the debtor’s intent. This landmark decision significantly impacts the UAE’s Islamic finance sector and customer protection standards.

Court’s Definitive Stance on Islamic Banking Practices

The Court of Cassation declared that Islamic financial institutions operating fully or partially under Sharia law cannot impose late payment charges, even when labelled as “compensation” or under alternative terminology. The ruling states these restrictions apply to all debts arising from Sharia-compliant transactions, regardless of payment delay circumstances.

“Islamic financial institutions and Takaful companies that operate fully or partially in accordance with Islamic Sharia law are not permitted to impose late interest fees — whether labeled as compensation or by any other name,” the court declared, according to Emarat Al Youm.

The ruling establishes this principle as “a matter of public order” that courts must apply independently, superseding any contradictory previous decisions.

Background: Resolving Legal Contradictions

This decisive ruling emerged from a formal request by the Court of Cassation’s head to address inconsistencies in earlier judicial decisions. Previous courts had reached conflicting conclusions about whether Islamic financial institutions could legitimately charge late payment penalties as compensation for delayed obligations.

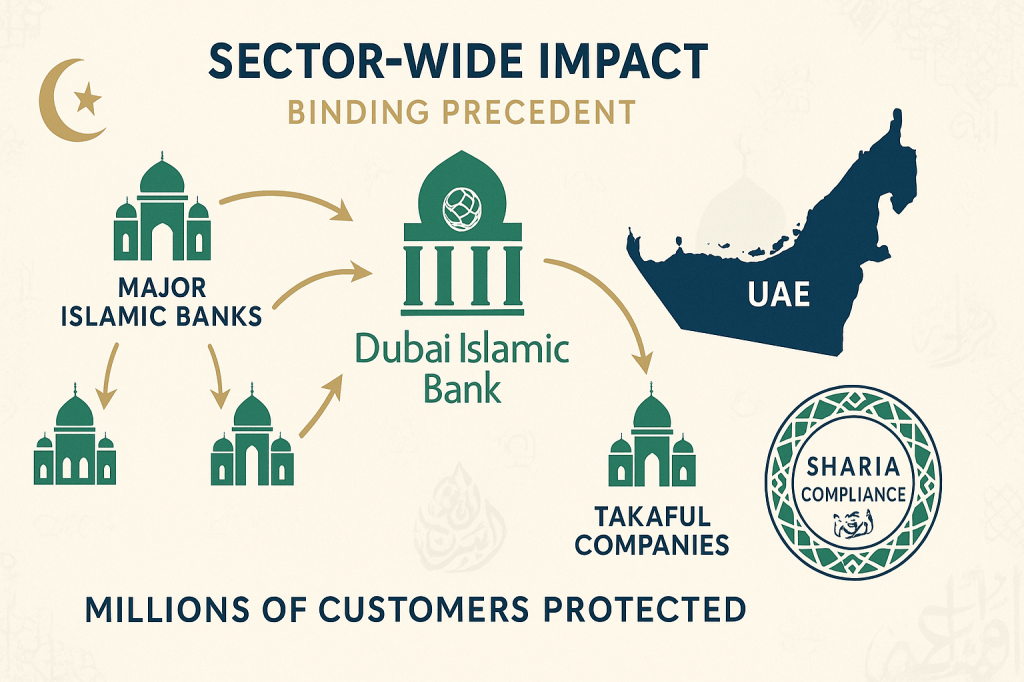

The matter was elevated to the General Assembly of the Court of Cassation for definitive interpretation under Article 20 of Law No. 13 of 2016, which governs Dubai’s judicial authority. This process creates binding precedent for future cases involving Islamic banking practices.

Impact on UAE’s Islamic Banking Sector

The ruling affects a substantial portion of the UAE’s financial services industry. Dubai Islamic Bank, one of the region’s largest Islamic financial institutions, alongside numerous other Sharia-compliant banks and Takaful companies must adjust their policies accordingly.

Key implications include:

For Islamic Banks

- Immediate cessation of late payment charges on existing accounts

- Revenue model adjustments to compensate for lost fee income

- Enhanced risk assessment procedures for credit facilities

- Revised contract terms for new customers

For Takaful Companies

- Policy adjustments for delayed premium payments

- Alternative collection mechanisms compliant with Sharia principles

- Revised customer communication strategies

Customer Protection Benefits

This ruling provides significant advantages for consumers using Islamic financial services:

Immediate Financial Relief

Customers with existing delayed payment obligations will no longer face additional charges, providing immediate financial relief for individuals and businesses experiencing cash flow challenges.

Enhanced Transparency

The prohibition eliminates ambiguity around compensation charges that some institutions previously imposed, creating clearer terms for Islamic banking customers.

Stronger Sharia Compliance

The ruling reinforces genuine Islamic banking principles, distinguishing these services from conventional banking practices that permit interest-based penalties.

Industry Adaptation Strategies

Islamic banks and Takaful companies must now develop alternative approaches to manage delayed payments whilst maintaining Sharia compliance:

Enhanced Due Diligence

Financial institutions may implement more stringent customer assessment procedures to minimize default risks upfront rather than relying on penalty charges as deterrents.

Alternative Collection Methods

Banks might develop Sharia-compliant incentive systems, such as early payment discounts or loyalty programmes, rather than punitive late fees.

Technology Integration

AI and digital banking solutions could help institutions better predict and prevent payment delays through predictive analytics and automated customer communications.

Broader Legal Implications

This ruling extends beyond individual customer relationships to affect commercial and corporate banking:

Business Financing

Companies utilizing Islamic financing facilities benefit from protection against late payment penalties, potentially improving cash flow management during economic uncertainties.

Real Estate and Development

Property developers and investors using Islamic banking products gain additional financial flexibility without facing penalty charges during project delays.

Trade Finance

International trade transactions using Islamic banking instruments receive enhanced protection from delay-related charges, supporting UAE’s position as a global trade hub.

Regional Influence and Standards

Dubai’s ruling may influence Islamic banking practices across the GCC region and globally. As a leading Islamic finance centre, UAE court decisions often serve as precedents for other jurisdictions offering Sharia-compliant financial services.

The decision reinforces the UAE’s commitment to authentic Islamic banking principles whilst protecting consumer interests, potentially attracting more customers seeking genuine Sharia-compliant financial services.

Future Considerations for Customers

Individuals and businesses considering Islamic banking services should understand both the benefits and responsibilities this ruling creates:

Advantages

- Protection from late payment charges

- Clearer contract terms

- Enhanced Sharia compliance assurance

Responsibilities

- Continued obligation to meet payment schedules

- Potential for alternative collection methods

- Possible adjustments to credit terms and conditions

Employment Impact on Financial Services

This regulatory change may influence career opportunities in Islamic banking, creating demand for professionals specializing in Sharia-compliant risk management and alternative revenue strategies.

Financial institutions may require additional expertise in developing innovative Islamic finance products that maintain profitability whilst adhering to enhanced regulatory standards.

Key Takeaway

Dubai’s Court of Cassation ruling prohibiting late payment charges by Islamic banks and Takaful companies represents a landmark decision strengthening consumer protection and Sharia compliance. This binding precedent eliminates ambiguous “compensation” charges, providing immediate financial relief for customers whilst requiring institutions to develop alternative, genuinely Islamic approaches to managing delayed payments.

Leave a comment