For many UAE residents, purchasing a vehicle represents one of their most significant financial decisions. Whether you’re considering a brand-new model or a pre-owned vehicle, understanding your financing options can save you thousands of dirhams whilst helping you secure the best possible deal.

From traditional bank loans to innovative credit card strategies, the UAE automotive financing landscape offers diverse pathways to car ownership. This comprehensive guide examines every major financing method available to residents, helping you make an informed decision that aligns with your financial goals.

Bank Loans: The Traditional Choice for UAE Car Buyers

Bank loans remain the most popular financing option amongst UAE residents, particularly for those with established banking relationships and strong credit profiles. According to Imad Hammad, Founder and CEO of CarSwitch, “Banks are often the most competitive financing option, particularly if the buyer has a strong credit profile – reputable employer, lengthy employment period, good income, limited liabilities and no history of defaults.”

The competitive advantage becomes even more pronounced when you take time to research multiple institutions. “Though it does take a scan to find the most attractive bank for the particular buyer,” Hammad explains. This research phase proves crucial, as interest rates and terms can vary significantly between different financial institutions across the Emirates.

Second-Hand Vehicle Financing in the Growing Market

The pre-owned car market in the UAE has experienced remarkable expansion, creating parallel growth in used vehicle financing options. Neeraj Gupta, CEO at Policybazaar UAE, notes that “car financing is predominantly driven by bank loans, particularly for second-hand vehicles, which constitute a rapidly expanding segment of the market.”

This growth has prompted banks to adapt their services more effectively for the used car segment. “The growing second-hand car ecosystem has triggered a parallel rise in used car financing, with banks adapting to serve this segment more effectively,” Gupta adds.

Banks typically offer similar financing terms for used vehicles, though they may require additional documentation such as vehicle inspection reports and may cap the loan amount based on the car’s current market value rather than its original price.

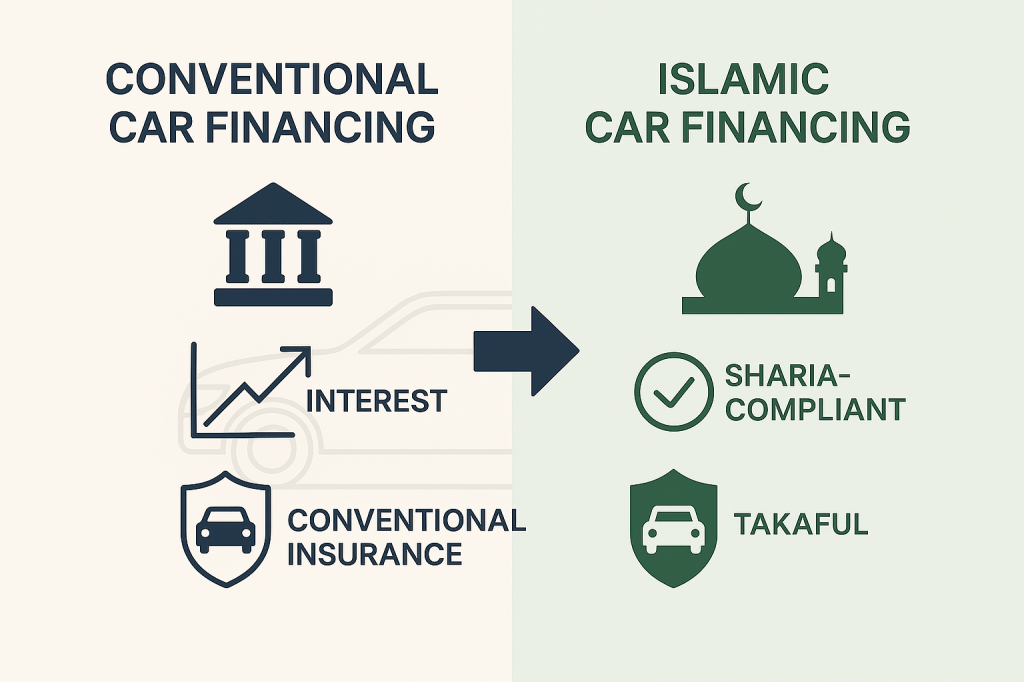

Islamic Financing: Sharia-Compliant Car Loans

For residents seeking Sharia-compliant financing options, Islamic car loans provide an alternative that adheres to religious principles whilst delivering similar practical benefits to conventional loans. The consumer experience remains largely consistent between Islamic and conventional financing options.

The primary distinction lies in the insurance requirement. Islamic financing mandates Takaful (Islamic insurance) instead of conventional insurance coverage. In Takaful, participants pool their contributions to mutually protect each other against loss or damage, based on ethical principles that align with Shariah law.

From a practical standpoint, the application process, approval criteria, and monthly payment structures mirror conventional loans, making the transition seamless for borrowers who prefer Sharia-compliant products.

Credit Card Financing: Emerging Trend for Smart Buyers

An increasingly popular strategy involves using credit cards as a financing tool, particularly those offering interest-free periods. This approach has gained traction as buyers seek more flexible payment solutions and potentially lower costs.

Hammad identifies two primary applications: “Sometimes it’s used in conjunction with financing to cover the initial downpayment, other times it’s to purchase directly from an end user who wants a cash deal (usually cheaper than buying from a dealership) especially for lower value cars.”

This strategy supports the growing trend towards cost-conscious purchasing, where buyers gravitate towards used cars sold by private individuals to secure the best possible deals. Credit cards provide the flexibility to manage these cash transactions whilst potentially benefiting from rewards programmes or interest-free periods.

However, buyers should carefully calculate the total cost, including any cash advance fees, and confirm they can repay the balance before promotional periods expire.

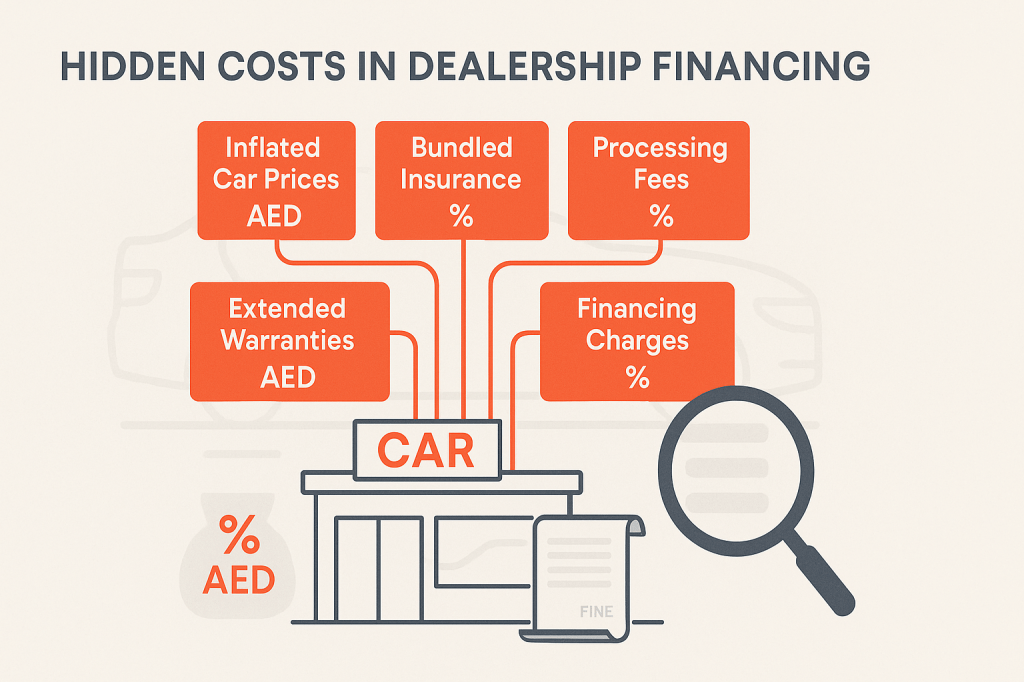

Dealership Financing: Convenience vs Cost Considerations

Dealership financing and leasing options continue gaining popularity, especially for new vehicle purchases. These programmes offer convenience by allowing buyers to complete their vehicle purchase and financing in a single location.

However, financial experts consistently recommend approaching dealership offers with caution. Gupta warns that buyers should be particularly careful with dealership financing offers that advertise zero per cent interest or no down payment requirements.

“Financing deals that advertise zero per cent interest often include hidden costs, either in the form of inflated car prices or bundled insurance add-ons,” Gupta explains. “So, while the sticker offer may look cheaper, the total cost of ownership might be higher.”

The key lies in transparency and careful examination of all terms. “Transparency in pricing and reading the fine print are essential to identifying the most economical choice,” he emphasises.

Trade-In and Private Sale Strategies

For current vehicle owners, two primary options exist for disposing of their existing car: trading in with a dealership or selling privately through online platforms.

The UAE market offers numerous car-selling portals including Dubizzle, Carbuyingpeople, and SellyAnyCar, each providing different advantages and fee structures. The optimal choice depends on your priorities regarding convenience, final sale price, and time investment.

Financial experts recommend obtaining a trade-in quote from your dealer first, then comparing this figure with potential returns from private sale platforms. This comparison helps determine whether the convenience of a trade-in justifies the typically lower price, or whether private sale efforts will yield significantly better returns.

Private sales generally offer higher returns but require more time and effort, including handling inquiries, arranging viewings, and completing paperwork independently.

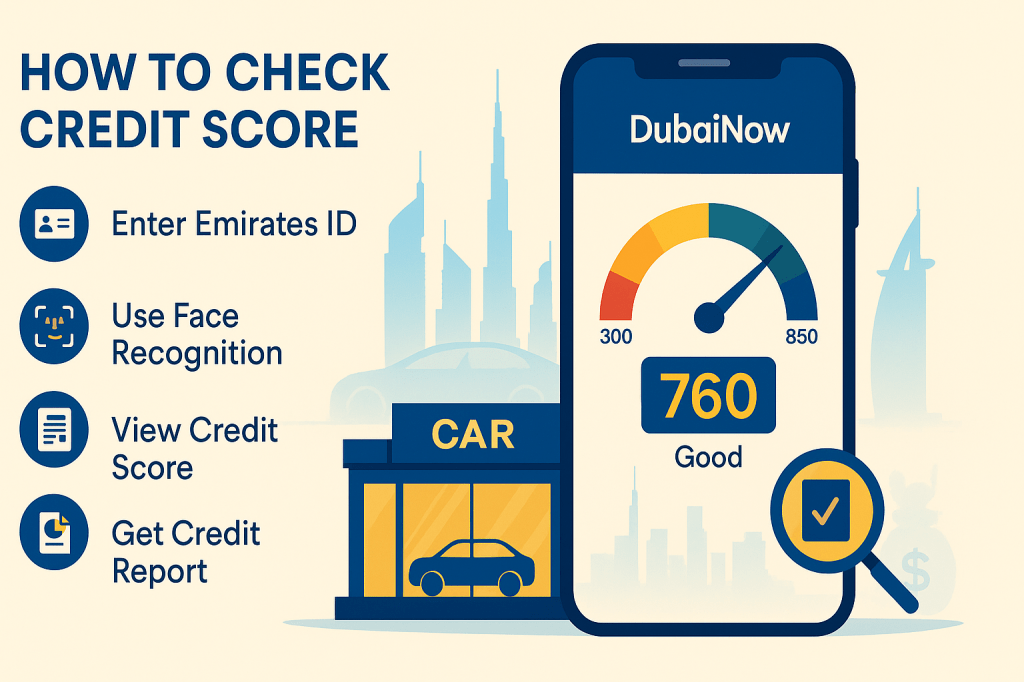

Credit Scores and Employment Status Impact

In the UAE, credit scores and employment status play central roles in determining loan approval and applicable interest rates. The financial system relies heavily on Etihad Credit Bureau (ECB) reports to assess borrower creditworthiness.

A strong credit history with consistent repayment patterns can significantly increase approval chances and unlock preferential interest rates. Conversely, poor credit scores may result in higher rates or complete rejection of loan applications.

Recent technological developments have made credit score monitoring more accessible. UAE residents can now obtain their credit scores instantly through the DubaiNow app, thanks to a partnership with the ECB. This accessibility allows potential car buyers to check their credit status before applying for financing, potentially improving their negotiating position.

Determining the Most Cost-Effective Option

The most economical financing choice depends on multiple interconnected factors, primarily credit score, down payment capacity, and vehicle selection (new versus used). Financial experts consistently indicate that bank loans with solid credit profiles and sizeable upfront payments tend to offer the most cost-effective solutions.

Gupta notes that “for buyers with excellent credit history, some banks even offer promotional low-rate loans that are more affordable than dealership offers, especially when factoring in the actual vehicle value and long-term costs.”

These promotional rates often coincide with specific periods throughout the year, such as during automotive exhibitions or at the end of financial quarters when banks aim to meet lending targets.

Insurance Considerations and Online Comparisons

An often-overlooked aspect of car financing involves insurance planning and cost management. Regardless of your chosen financing method, comprehensive insurance remains mandatory in the UAE, and the cost can significantly impact your total ownership expenses.

Online insurance comparison platforms offer substantial advantages over traditional purchasing methods. These platforms enable buyers to evaluate policies from multiple insurers, customise coverage based on individual requirements, and avoid inflated premiums or unnecessary add-ons.

This level of transparency and flexibility typically isn’t available when purchasing insurance through dealerships, where bundled packages may include coverage you don’t require at premium prices.

Professional Financial Planning Strategies

Successfully financing a car purchase in the UAE requires strategic planning that considers your broader financial picture. Financial experts recommend establishing a budget that accounts for the total cost of ownership, including insurance, registration, maintenance, and potential depreciation.

Consider the impact of monthly payments on your debt-to-income ratio, particularly if you’re planning other major purchases such as property investment or have existing loan commitments. UAE banks typically evaluate total debt obligations when considering new loan applications.

For expatriate professionals, currency fluctuation considerations may also play a role, especially if your income originates from sources outside the UAE or if you’re planning to relocate within your loan term.

Digital Innovation in Car Financing

The UAE’s automotive financing sector continues evolving through digital innovation and streamlined application processes. Many banks now offer pre-approval services that allow potential buyers to understand their financing capacity before visiting dealerships, strengthening their negotiating position.

Mobile banking applications frequently feature dedicated auto loan sections with calculators, comparison tools, and instant approval capabilities for qualifying applicants. These technological advances reduce processing times and improve transparency throughout the financing journey.

Some institutions have partnerships with major dealerships, enabling integrated financing applications that can be completed during the vehicle selection process whilst maintaining competitive rates.

Key Takeaway

The best car financing method in the UAE depends on your credit profile, down payment capacity, and vehicle choice. Bank loans typically offer the most competitive rates for buyers with strong credit histories, whilst credit cards can provide flexibility for smaller purchases or down payments. Always compare total costs including insurance, avoid dealership financing with hidden fees, and leverage your credit score through the DubaiNow app to secure optimal terms.

Leave a comment