Key Takeaway: Oman becomes the first GCC nation to implement personal income tax from January 1, 2028, targeting only the top 1% of earners with a 5% rate on incomes above OMR42,000 ($109,230) annually, supporting Vision 2040’s economic diversification goals.

The Gulf Cooperation Council’s tax-free employment landscape faces its first major transformation as Oman prepares to implement the region’s inaugural personal income tax system. This groundbreaking development marks a strategic shift in how Gulf nations approach revenue generation and economic sustainability.

Historic Tax Implementation Timeline

Oman’s Personal Income Tax Law, enacted through Royal Decree No 56/2025, represents a carefully planned transition spanning three years of preparation. The 76-article legislation across 16 chapters reflects comprehensive planning to address economic and social considerations whilst maintaining the Sultanate’s competitive position.

The law takes effect from January 1, 2028, providing businesses and individuals ample time to prepare for this transformation. This extended timeline demonstrates Oman’s commitment to smooth implementation without disrupting existing economic activities or employment patterns.

Karima Mubarak Al Saadi, Director of the Personal Income Tax Project, confirms that all necessary preparations have been completed well in advance. An electronic system developed by the Tax Authority promotes voluntary compliance and integrates with relevant government departments for accurate income calculation and verification.

Targeted High-Earner Focus

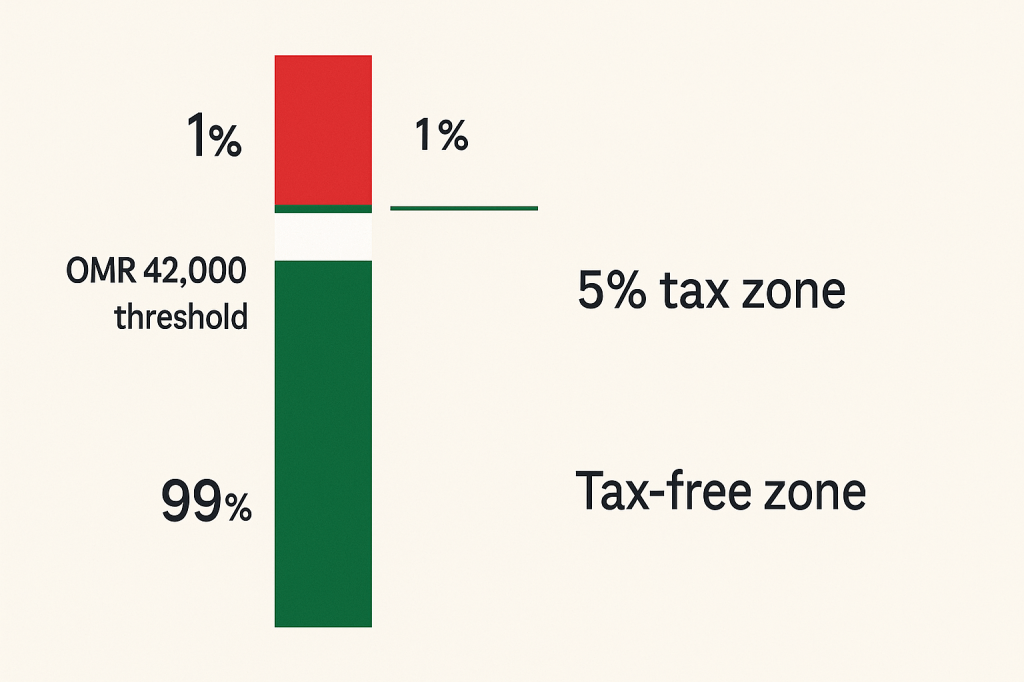

The new tax system demonstrates surgical precision in its application, affecting only approximately 1% of Oman’s population. Individuals earning above OMR42,000 ($109,230/AED401,160) annually will face a 5% tax rate on their income exceeding this threshold.

This selective approach ensures that 99% of Oman’s population remains unaffected by the new tax regime. The high exemption threshold reflects careful consideration of social and economic factors, maintaining the Sultanate’s attractiveness for middle-income professionals whilst generating revenue from high earners.

The Authority conducted extensive studies using income data from various government entities to establish this exemption threshold. This data-driven approach aimed to balance revenue generation with minimal social disruption, ensuring the tax system supports rather than hinders economic growth.

Comprehensive Deduction Framework

The tax law includes substantial deductions and exemptions addressing social considerations specific to Oman’s society. These provisions recognise the importance of education, healthcare, and cultural obligations in determining taxable income.

Key deduction categories include:

- Educational expenses for dependents

- Healthcare costs and medical treatment

- Inheritance-related expenses

- Zakat and religious obligations

- Charitable donations and community contributions

- Primary housing and accommodation costs

- Other socially relevant factors

These deductions demonstrate the government’s commitment to protecting essential family expenses from taxation whilst maintaining revenue objectives.

Vision 2040 Economic Diversification

The Personal Income Tax Law directly supports Oman Vision 2040’s strategic objectives of diversifying income sources and reducing dependence on oil revenues. The ambitious targets include achieving 15% of GDP from non-oil sources by 2030 and 18% by 2040.

This taxation framework forms part of broader economic reforms designed to create sustainable revenue streams independent of volatile oil markets. The approach aligns with global trends where resource-rich nations seek to build resilient economies capable of thriving regardless of commodity price fluctuations.

The revenue generated will specifically finance parts of the social protection system, creating a direct link between high earners’ contributions and societal benefits. This approach promotes wealth redistribution whilst maintaining incentives for economic success and professional advancement.

Regional Tax Landscape Context

Oman’s personal income tax introduction occurs within a broader pattern of Gulf tax reforms. Other GCC nations have already implemented various tax measures to diversify revenue streams whilst maintaining competitive business environments.

The UAE introduced federal corporate tax on business profits at 9%, designed to maintain its business-friendly reputation whilst generating additional revenue. Saudi Arabia imposes corporate income tax at 20%, whilst Qatar levies 10% on corporate profits.

Value Added Tax (VAT) at 5% has been implemented across the UAE, Saudi Arabia, Oman, and Bahrain, affecting goods and services rather than personal income. This regional coordination demonstrates collective recognition of the need for tax system modernisation.

Impact on Regional Employment Markets

The introduction of personal income tax in Oman may influence regional employment patterns, particularly for high-earning professionals. UAE’s continued tax-free salary structure becomes more attractive relative to Oman’s new tax regime.

This development could potentially drive talent migration within the GCC, as professionals earning above the OMR42,000 threshold may consider relocating to maintain tax-free income. However, Oman’s comprehensive deduction system may offset this effect for many individuals.

The selective nature of the tax, affecting only 1% of the population, minimises disruption to Oman’s general labour market. Most expatriate workers and local employees will continue operating under the traditional tax-free system that has characterised Gulf employment.

Technology Infrastructure and Compliance

The Tax Authority has developed sophisticated electronic systems to facilitate voluntary compliance and accurate tax assessment. These systems integrate with relevant government departments, enabling comprehensive income verification and streamlined declaration processes.

This technological infrastructure represents significant investment in modern tax administration capabilities. The system aims to minimise compliance burdens whilst ensuring accurate assessment and collection of taxes from eligible individuals.

The Authority has also enhanced workforce capabilities through specialised training programmes aligned with tax implementation requirements. This preparation ensures smooth system operation from the January 2028 launch date.

Social Justice and Wealth Redistribution

The tax system explicitly aims to promote wealth redistribution among societal segments whilst enhancing social justice. This approach reflects growing global recognition of tax policy’s role in addressing income inequality and funding social development.

By targeting only the highest earners whilst providing comprehensive deductions for social expenses, the system maintains incentives for economic success whilst ensuring wealthy individuals contribute to broader societal development.

The direct link between tax revenue and social protection system funding creates transparent connections between individual contributions and community benefits. This approach may enhance public acceptance of the new tax regime.

Comparative Analysis with UAE Systems

The contrast between Oman’s new personal income tax and UAE’s continued tax-free salary structure creates interesting dynamics within the GCC employment market. High earners may need to recalculate the relative attractiveness of different Gulf destinations.

For individuals earning below OMR42,000 annually, Oman’s employment proposition remains unchanged. However, senior executives, specialist professionals, and business leaders may find UAE positions more financially attractive post-2028.

This development may intensify competition among GCC nations for top talent, potentially driving salary increases or enhanced benefit packages to offset tax implications. UAE employers already offering comprehensive benefit packages may gain additional competitive advantages.

Preparation Strategies for Affected Individuals

High-earning professionals in Oman should begin preparing for the 2028 tax implementation through strategic financial planning. Understanding available deductions and exemptions becomes crucial for minimising tax liabilities whilst maintaining compliance.

Key preparation areas include:

- Documenting eligible educational and healthcare expenses

- Organising charitable giving and zakat contributions

- Reviewing housing and accommodation arrangements

- Consulting tax professionals for optimisation strategies

- Understanding compliance requirements and deadlines

Early preparation enables individuals to structure their finances advantageously whilst ensuring full compliance with the new regulations.

Regional Economic Implications

Oman’s pioneering approach to personal income tax may influence other GCC nations’ long-term tax strategies. As oil revenues face ongoing volatility, other Gulf states may consider similar measures to diversify income sources.

However, the competitive dynamics within the GCC for attracting international talent and investment may moderate this trend. Nations implementing personal income tax risk losing competitive advantages in global talent markets unless accompanied by offsetting benefits.

The success or challenges of Oman’s implementation will likely influence regional decisions about personal taxation. Positive outcomes may encourage similar measures, whilst difficulties could reinforce preferences for alternative revenue sources.

Professional Sector Considerations

Specific professional sectors may face varying impacts from the new tax regime. High-earning roles in finance, oil and gas, consulting, and senior management positions will be most affected by the 5% tax rate.

Professional service firms may need to adjust compensation structures to maintain competitive positions relative to UAE and other GCC alternatives. This could include gross-up provisions or enhanced benefits to offset tax impacts.

The comprehensive deduction framework may particularly benefit professionals with families, given allowances for education and healthcare expenses. Single high earners without significant deductible expenses may face the full impact of the 5% rate.

Implementation Monitoring and Adjustments

The Tax Authority’s comprehensive preparation includes systems for monitoring implementation effectiveness and making necessary adjustments. This approach recognises that tax systems require ongoing refinement based on practical experience.

Early implementation phases will likely focus on voluntary compliance and education rather than aggressive enforcement. This approach allows individuals and employers time to adapt whilst identifying any system improvements needed.

Regular reviews of the exemption threshold and tax rate may occur based on economic conditions and revenue requirements. The system’s flexibility enables adjustments supporting both fiscal objectives and economic competitiveness.

Future GCC Tax Evolution

Oman’s personal income tax implementation represents a potential watershed moment for Gulf tax policy. Other GCC nations will closely monitor outcomes to inform their own long-term revenue strategies.

The regional trend toward tax diversification reflects recognition that sustainable economic development requires multiple revenue sources. However, maintaining competitive advantages in attracting international talent and investment remains crucial.

Future developments may include regional coordination on tax policies to prevent destructive competition whilst ensuring adequate revenue generation. This balance between fiscal needs and economic competitiveness will shape Gulf taxation evolution.

The success of Oman’s targeted approach—affecting only 1% of the population whilst generating meaningful revenue—may provide a model for other nations considering personal taxation introduction.

Leave a comment