The UAE has introduced sweeping changes to its financial regulatory framework. President Sheikh Mohamed bin Zayed Al Nahyan issued a federal decree-law governing the Central Bank, financial institutions, and insurance activities – marking a significant shift in how banks and financial entities operate across the Emirates.

This legislation brings stricter penalties, enhanced consumer protection, and new compliance requirements that affect everyone from major banks to individual borrowers. Here’s what you need to know about these changes.

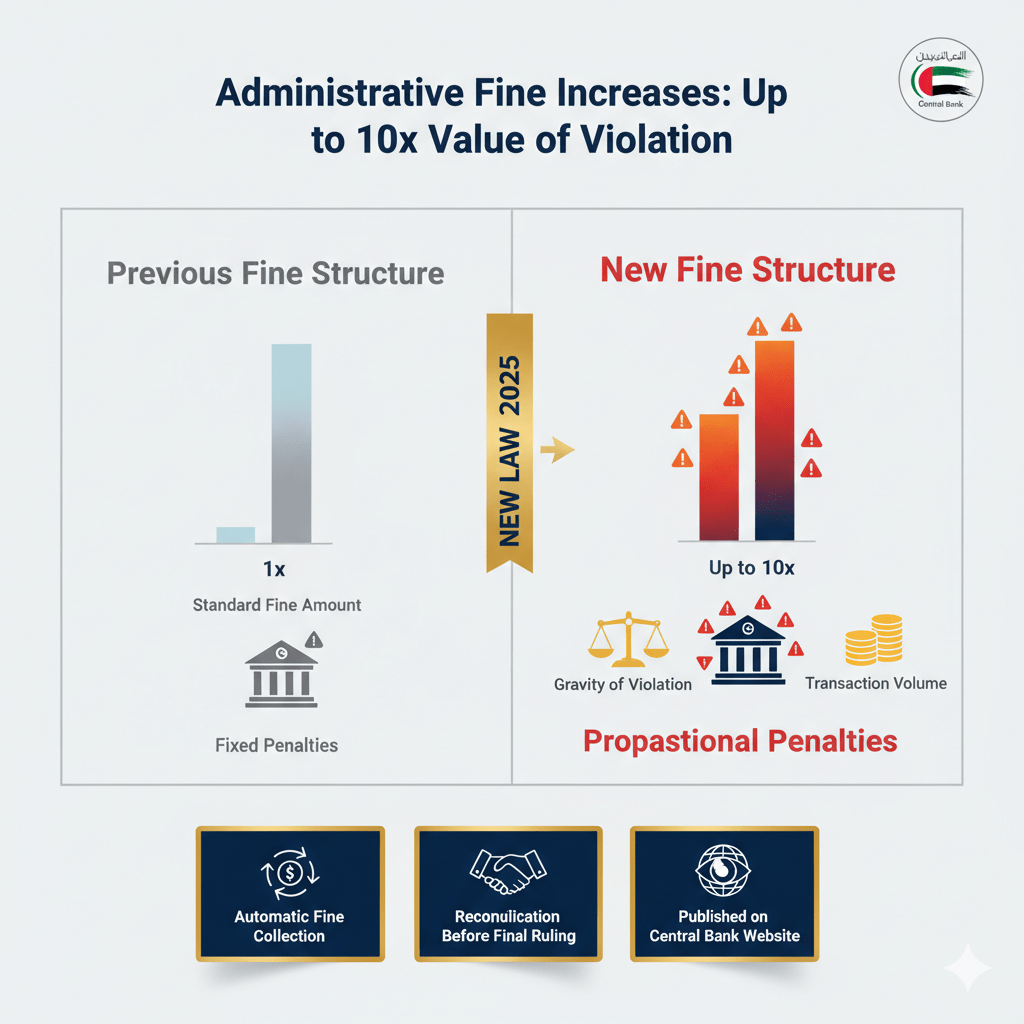

Increased Penalties for Financial Violations

The most striking change involves administration fines. Financial institutions now face penalties up to ten times the value of violations – a substantial increase from previous regulations.

This escalation reflects the government’s commitment to maintaining financial system integrity. The severity of fines now corresponds directly to two factors: the gravity of violations and the transaction volume involved.

How the New Fine Structure Works

Previously, financial penalties followed fixed schedules regardless of violation scale. The new framework introduces proportional penalties that scale with both the severity and scope of infractions.

For institutions handling large transaction volumes, minor compliance failures could result in significant financial consequences. This approach aims to make penalties meaningful deterrents rather than routine business costs.

The Central Bank will publish penalty settlements on its official website, introducing transparency into enforcement actions. This public disclosure serves dual purposes: holding institutions accountable whilst informing consumers about regulatory compliance records.

Automatic Fine Debiting and Reconciliation Options

Financial institutions face automatic debiting of imposed fines – eliminating delays in penalty collection. However, the law provides a reconciliation pathway allowing institutions to settle violations before final judicial rulings.

This provision offers institutions opportunities to address compliance issues proactively, potentially reducing financial impact through early resolution.

Enhanced Consumer Protection Measures

The legislation consolidates complaints and dispute resolution functions for banking and insurance customers. Previously, different entities handled various financial complaints, creating confusion for consumers seeking redress.

Under the new framework, customers access unified complaint channels regardless of whether issues involve banks or insurance companies. This streamlining should accelerate resolution times and improve consumer experience.

For UAE residents and expatriates managing banking relationships, this change provides clearer pathways for addressing service disputes. Understanding your rights under the UAE banking regulations becomes increasingly important as consumer protection strengthens.

Digital Transformation and Financial Access Requirements

Licensed financial institutions must now provide all community members with proper banking and financial services. This mandate aligns with the UAE’s digital transformation objectives and financial innovation initiatives.

Banks cannot restrict service access arbitrarily – they must facilitate financial inclusion whilst maintaining security standards. This requirement particularly benefits residents navigating employment transitions who previously faced banking access challenges.

Early Intervention Framework for Financial Stability

The law establishes proactive measures enabling early intervention when licensed institutions show signs of financial deterioration. Rather than waiting for crises to develop, regulators can now implement preventive actions.

These measures protect depositors and maintain confidence in the financial system. For individuals and businesses holding deposits or maintaining financial relationships with UAE institutions, this framework provides additional security layers.

Currency Stability and Foreign Exchange Management

The Central Bank’s mandate explicitly includes maintaining national currency stability, protecting financial system stability, and prudently managing foreign exchange reserves.

These responsibilities directly affect expatriates and businesses dealing with currency exchange, international transfers, and foreign currency accounts. The UAE dirham’s peg to the US dollar remains a cornerstone of this stability framework.

New Guarantee Requirements for Personal Loans

Financial institutions must now obtain and maintain adequate guarantees for facilities provided to natural persons and sole proprietorships. This requirement affects personal loans, credit facilities, and business financing.

Borrowers should expect more stringent collateral requirements when applying for loans or credit lines. Banks will likely request additional documentation or security to comply with these guarantee mandates.

For entrepreneurs and sole proprietors seeking business financing, understanding these requirements becomes crucial for successful loan applications.

What This Means for Banking Customers

Stronger Consumer Rights: Unified complaint systems provide clearer paths for dispute resolution.

Service Access: Banks must facilitate financial services for all community members, potentially expanding options for residents facing access challenges.

Transparency: Published penalty settlements allow customers to review institutions’ regulatory compliance history.

Tighter Lending: Expect more rigorous documentation requirements for personal loans and credit facilities due to enhanced guarantee requirements.

What This Means for Financial Institutions

Higher Compliance Costs: Increased penalties make violations significantly more expensive, necessitating stronger compliance frameworks.

Operational Changes: Unified consumer protection functions require adjustments to complaint handling procedures.

Early Warning Systems: Institutions must implement monitoring to detect financial deterioration signs before triggering regulatory intervention.

Digital Service Obligations: Banks must accelerate digital transformation efforts to meet expanded service access requirements.

Implementation Timeline

The law takes effect immediately following publication in the Official Gazette. Financial institutions must align operations with new requirements, whilst consumers can begin utilizing enhanced protection mechanisms.

Regulatory guidance from the Central Bank will clarify specific implementation details for various provisions.

Frequently Asked Questions

How do the increased fines affect individual banking customers?

Individual customers aren’t directly subject to these administrative fines – they apply to financial institutions. However, customers benefit indirectly through improved compliance and service standards as banks strengthen operations to avoid penalties.

Can I check if my bank has been fined under the new law?

Yes. The Central Bank will publish penalty settlements on its official website, providing transparency into enforcement actions against licensed institutions. This allows customers to review their bank’s regulatory compliance record.

What happens if I have a complaint against my bank or insurance company?

The new law establishes unified complaint and dispute resolution functions. Contact your institution’s customer service first, then escalate to the Central Bank’s consumer protection department if unresolved. The streamlined process should provide clearer resolution pathways.

Will loan approval become more difficult under the new guarantee requirements?

Possibly. Banks must now obtain adequate guarantees for facilities to natural persons and sole proprietorships. This may result in stricter collateral requirements, more documentation requests, or higher income verification standards for personal loans.

Does this law affect existing loans and banking relationships?

Existing agreements remain valid under their original terms. However, renewal applications or new facilities will fall under the updated guarantee requirements. Banks may request additional documentation when existing facilities come up for renewal.

Key Takeaway

The UAE’s new Central Bank law introduces significant changes affecting financial institutions and customers. Penalties for violations increase up to tenfold, whilst consumers gain enhanced protection through unified complaint systems. Financial institutions must provide broader service access aligned with digital transformation goals, implement early warning systems for financial stability, and maintain adequate guarantees for personal lending. These changes strengthen the UAE’s financial system integrity whilst expanding consumer rights and service accessibility.

Further Reading

- Can UAE Residents Keep Bank Accounts After Visa Cancellation?

- UAE Bank Fraud Compensation: When Banks Must Refund Scam Victims

- UAE Visa Grace Period: How Long Can You Stay After Visa Cancellation?

- Dubai Security Deposit Rules: When Landlords Must Issue Full Refunds

- How to Easily Get VAT Refunds in the UAE

Leave a comment