Major Banks to Increase Minimum Balance Requirements from Dh3,000 to Dh5,000

Several major banks operating in the UAE are preparing to implement significant changes to their minimum balance requirements for current accounts. Starting June 1, these financial institutions plan to increase the minimum required balance from Dh3,000 to Dh5,000, aligning with the UAE Central Bank’s regulations on personal loans.

According to a survey conducted by ‘Emarat Al Youm‘, at least one leading bank has already adopted the new minimum balance threshold, with others expected to follow suit shortly. This adjustment represents the first major change to account balance requirements since 2011, when the current Dh3,000 threshold was established for personal loan-linked accounts.

New Fee Structure and Exemption Criteria

The revised policy will directly affect account holders across the country, introducing a higher financial threshold for maintaining bank accounts without incurring penalties. Under the new guidelines, customers who fail to maintain the Dh5,000 minimum balance will face a monthly fee of Dh25, unless they qualify for an exemption.

Banks have established several exemption paths to help customers avoid these fees:

- Maintain a substantial total account balance of Dh20,000 or more across all accounts

- Transfer a monthly salary of at least Dh15,000

- Hold additional financial products with the bank (for those with salaries between Dh5,000 and Dh14,999), such as:

- An active credit card

- An overdraft facility

- A loan

For customers who transfer a monthly salary below Dh5,000 and don’t meet additional criteria, the monthly fee will apply automatically. Account holders who don’t fit into any exemption category could face even steeper charges, with some banks potentially imposing fees of Dh100 or Dh105 per month, depending on the account type.

Historical Context of Minimum Balance Requirements

The UAE’s banking minimum balance requirements have remained relatively stable since 2011, when the Central Bank established Dh3,000 as the standard threshold for personal loan-linked accounts. This long-standing policy provided customers with a consistent benchmark for managing their finances.

Minimum balance requirements serve multiple purposes within the banking system. They help financial institutions maintain steady cash reserves, offset account management costs, and encourage customers to maintain higher deposit levels. From the banks’ perspective, these requirements also facilitate better financial planning and liquidity management.

The Changing Banking Landscape in the UAE

The UAE banking sector continues to evolve rapidly, with a growing emphasis on digital services and improved customer experiences. While increasing minimum balance requirements, many banks are simultaneously expanding their digital offerings, creating a more convenient but potentially more costly banking environment.

The banking landscape in the UAE features a mix of local and international financial institutions. Major players include Emirates NBD, First Abu Dhabi Bank, Abu Dhabi Commercial Bank, Dubai Islamic Bank, and Mashreq Bank, alongside international entities like HSBC, Standard Chartered, and Citibank.

Many banks are expected to implement the new minimum balance requirements uniformly across their product lines, affecting both existing and new customers. However, the specific implementation details and potential grace periods may vary between institutions.

Impact on Different Customer Segments

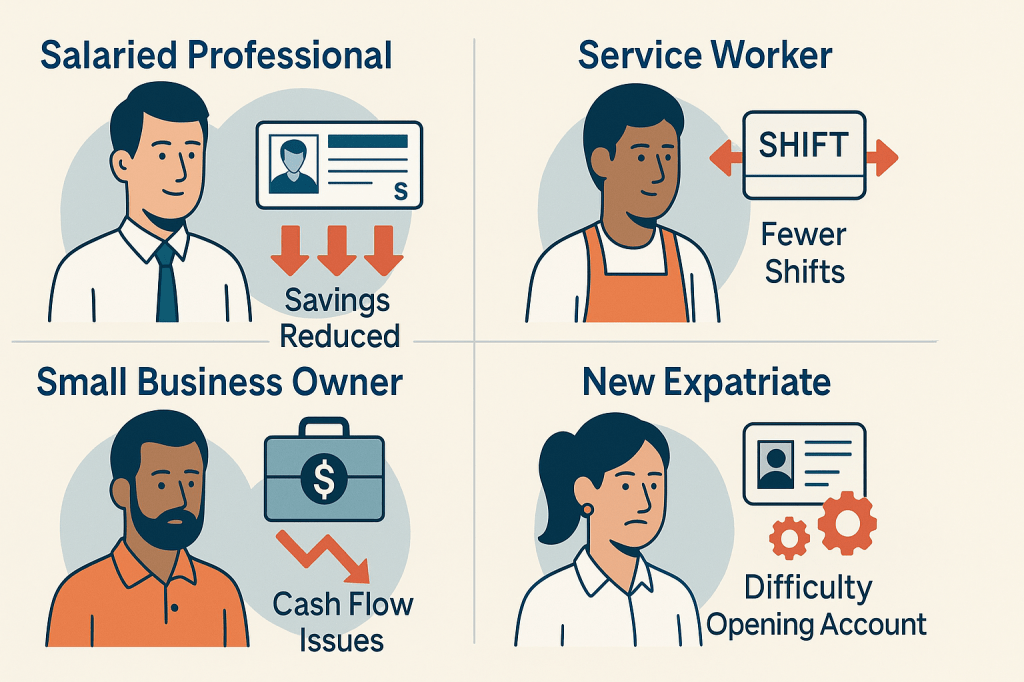

Salaried Professionals

For employees earning above Dh15,000 monthly, the new requirements will have minimal impact as their salary transfers will qualify them for fee waivers. Those earning between Dh5,000 and Dh14,999 will need to maintain active credit cards or other banking products to avoid fees.

Lower-Income Earners

The changes will most significantly affect those earning below Dh5,000 monthly, who will now face a higher threshold to avoid the Dh25 monthly fee. This group includes many service industry workers, entry-level employees, and part-time staff.

Small Business Owners and Freelancers

Entrepreneurs and self-employed individuals without regular salary transfers may find it more challenging to maintain the required minimum balance, potentially increasing their banking costs unless they can maintain the Dh20,000 total relationship balance.

Expatriates and New Residents

Newcomers to the UAE who are establishing their financial footing may struggle with the higher minimum balance requirement initially, particularly if they are settling in and managing relocation expenses.

Alternatives to Traditional Banking Options

As minimum balance requirements increase, some consumers may consider alternative banking solutions:

Zero-Balance Accounts

Several UAE banks offer zero-balance accounts, particularly for salary transfer customers. These accounts typically don’t require a minimum balance but may have other conditions such as regular salary transfers or limited transaction capabilities.

Digital Banking Options

Financial technology platforms and digital banks operating in the UAE often provide more flexible minimum balance requirements or none at all, making them attractive alternatives for customers seeking to avoid traditional banking fees.

Islamic Banking Alternatives

Some Islamic banking products offer different fee structures and may provide more accessible options for customers concerned about the increased minimum balance requirements.

Expert Perspectives on the Changes

Financial analysts suggest that the increase in minimum balance requirements reflects broader economic pressures and the banking sector’s need to enhance revenue streams. While potentially challenging for some customers, these changes align with the industry’s focus on profitability and sustainable growth.

Banking experts recommend that customers:

- Review their current account agreements and fee structures

- Explore consolidating accounts to meet the higher threshold

- Consider setting up automatic transfers to maintain the minimum balance

- Evaluate whether their current bank still offers the best value under the new requirements

Steps to Manage Your Finances Under the New Requirements

To navigate these changes effectively, consider the following strategies:

1. Assess Your Banking Needs

Review your transaction patterns, average balance, and banking habits to determine if your current account still meets your needs under the new requirements.

2. Explore Fee Waiver Options

Contact your bank to understand all possible ways to qualify for fee waivers, including total relationship balances, salary transfers, or additional product relationships.

3. Compare Account Options

Research different banks and account types to find options with more favorable terms, potentially including digital banks and fintech alternatives.

4. Set Up Balance Alerts

Establish notifications for when your account approaches the minimum threshold to avoid unexpected fees.

5. Consider Account Consolidation

If you maintain multiple accounts across different banks, consolidating them might help you reach the minimum balance requirement more easily.

Central Bank Regulations and Consumer Protection

The UAE Central Bank continues to play a vital role in regulating the banking sector, balancing the need for financial stability with consumer protection considerations. While banks have the autonomy to establish their fee structures, they must adhere to Central Bank guidelines regarding transparency and customer communication.

According to Article 9 of the Central Bank Rulebook on bank accounts and related fees, banks may set minimum credit balances for accounts and impose charges if such minimums are not maintained. However, banks must clearly disclose these requirements and associated fees to customers.

Consumers who believe their banks are not implementing these changes transparently can file complaints with the UAE Central Bank, which maintains robust consumer protection mechanisms.

Looking Ahead: Future Banking Trends in the UAE

The increase in minimum balance requirements reflects broader trends in the UAE banking sector, including:

- Greater emphasis on premium and priority banking services

- Expansion of digital banking capabilities

- More customized financial products based on customer segments

- Increased competition from fintech startups and digital-only banks

As the UAE continues to develop as a global financial hub, banks are likely to introduce more sophisticated pricing models that balance accessibility with profitability. Customers who stay informed and proactively manage their banking relationships will be best positioned to navigate these evolving requirements.

Key Takeaway

UAE banks are raising the minimum account balance requirement from Dh3,000 to Dh5,000 starting June 1, imposing a Dh25 monthly fee for non-compliance unless customers meet specific exemption criteria such as maintaining a Dh20,000 total balance or transferring a monthly salary of at least Dh15,000. This significant change, the first since 2011, will primarily impact lower-income earners, while introducing consumers to consider alternatives like zero-balance accounts or digital banking platforms.

FAQs About the New Minimum Balance Requirements

When will the new minimum balance requirements take effect?

The new minimum balance requirements are scheduled to take effect on June 1, 2025, although implementation dates may vary slightly between banks.

Will existing accounts be grandfathered under the old requirements?

Most banks are expected to apply the new requirements to both existing and new accounts. However, certain premium or long-standing customers might receive special considerations or grace periods.

How will I know if my bank is changing its minimum balance requirement?

Banks are required to notify customers of any changes to terms and conditions, including minimum balance requirements. Watch for communications via email, SMS, mobile banking notifications, or traditional mail.

Can I switch to a different account type to avoid the higher minimum balance?

Many banks offer various account types with different requirements. Contact your bank to explore alternative account options that might better suit your financial situation.

What happens if my balance falls below the minimum requirement for just a few days?

Most banks assess minimum balance requirements based on the lowest balance during the month or a specific period. Even if your balance falls below the minimum for a short time, you may still incur the fee unless your account qualifies for an exemption.

Are there any banks not implementing these changes?

While the trend appears to be industry-wide, some banks may choose to maintain lower minimum balance requirements as a competitive advantage. Research different banking options to find institutions offering more favorable terms.

How do these changes affect joint accounts?

Joint accounts will typically be subject to the same minimum balance requirements as individual accounts, but both account holders may pool their resources to meet the threshold.

Can I combine balances across multiple accounts to meet the minimum requirement?

Some banks consider your total relationship balance across all accounts when determining fee waivers. Check with your specific bank to understand their policies on combined balance calculations.

Leave a comment