Last updated: 8 April 2025

The UAE has introduced significant corporate tax updates that provide foreign investors with enhanced flexibility and clarity regarding their financial obligations. These timely changes, arriving amid global market uncertainties triggered by new US tariffs under the Trump administration, position Dubai as an increasingly attractive destination for international capital. Whether you’re considering UAE investment opportunities or already managing assets in the Emirates, these regulatory refinements offer substantial advantages that could significantly impact your investment strategy and tax liabilities in 2025.

UAE’s Strategic Tax Updates: Responding to Global Investment Shifts

The UAE government has recently issued two critical updates to its corporate tax framework specifically targeting foreign investment funds. These changes emerge at a pivotal moment in global economics, as investors seek stability amid shifting trade policies.

Key Changes for Foreign Investors

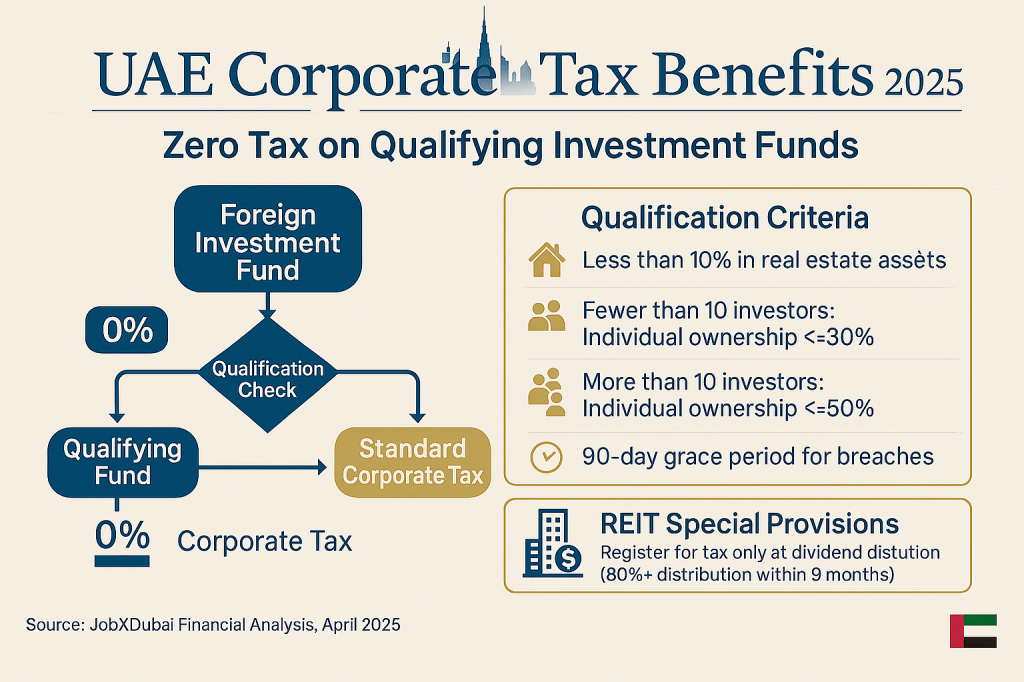

The updated regulations provide essential clarity on qualifying investment funds, offering zero corporate tax rates under specific conditions:

- Investment funds meeting certain criteria qualify for complete corporate tax exemption

- New guidelines provide precise thresholds for real estate investments and ownership structures

- Grace periods introduced for ownership breaches, reducing compliance risks

- Special provisions for Real Estate Investment Trusts (REITs) that simplify tax obligations

These measures arrive at a critical juncture as investors reassess global portfolios in response to new US tariff policies under the Trump administration.

“The UAE has captured the moment,” notes a market analyst. “You’ve got global investors who fear what will happen to their investments—and they want to see pockets of market stability. The UAE has provided extra reassurance to foreign investors wanting to come in and whether they are eligible for tax or not.”

Qualifying Fund Criteria: Zero Corporate Tax Requirements

The UAE’s tax authorities have established specific parameters for investment funds to qualify for corporate tax exemption status. Understanding these criteria is essential for investment planning.

Qualification Requirements for Tax Exemption

To qualify for zero corporate tax rates, investment funds must meet several precisely defined conditions:

- Real estate threshold: Less than 10% of the fund’s assets must be invested in real estate

- Investor number limitations: For funds with fewer than 10 investors, individual ownership interest must be less than 30%

- Larger fund provisions: For funds with more than 10 investors, the ownership threshold is capped at less than 50%

- Breach tolerance: An ‘ownership breach’ is not applicable for the first 2 years provided it wasn’t intentional

- Remediation period: Subsequent breaches benefit from a 90-day grace period for rectification

“The new UAE rules are favorable for foreign investors as long as the investment fund qualifies for corporate tax exempt status,” explains Girish Chand, Senior Partner at MCA Gulf. “If we assume a foreign investor has funds in a qualifying investment fund—then the income generated by the fund would be exempt from Corporate Tax provided it fulfills the exempt condition. Which also means the share of income earned by the foreign investor would be exempt as well.”

Tax Implications: Exemptions vs. Obligations

Understanding when tax obligations apply versus when exemptions are available is crucial for investment planning in the UAE market.

When Corporate Tax Applies

Tax liability is triggered only under specific circumstances:

- Non-qualifying funds: Investment vehicles that fail to meet exemption criteria

- Nexus establishment: When investors are deemed to have established a tax nexus in the UAE

- Registration requirements: Only investors in non-qualifying funds need to register for UAE corporate tax

“Only in cases where the fund does not fulfill the CT exempt conditions, would the investor be considered as having a ‘nexus’ in the UAE,” Chand clarifies. “Then, the investor would be required to register and pay UAE corporate tax.”

Special Provisions for Real Estate Investment

The updated regulations include targeted provisions for real estate investment, an area of significant interest for many international investors looking at the UAE market.

REIT-Specific Tax Benefits

Real Estate Investment Trusts receive special consideration under the new rules:

- Dividend distribution timing: Foreign investors in REITs that distribute 80% or more of their income within nine months of the financial year-end are only required to register for corporate tax on the date of the dividend distribution

- Reduced administrative burden: These provisions streamline compliance procedures for REIT investors

- Real estate investment clarity: Clearer guidelines on permissible real estate exposure for tax-exempt status

“What the new decisions do is reduce the compliance burden on foreign investors providing clarity and stability in attracting institutional investment into UAE real estate,” says Sameer Lakhani, Managing Director at Global Capital Partners. “It provides extra clarity on the leeway that foreign investors have in their ability to invest in UAE real estate. This will pave the way for greater institutional ownership.”

Comparative Advantage: UAE vs. Global Investment Destinations

These tax updates strengthen the UAE’s position relative to other investment destinations, particularly as global investors reassess their portfolios in response to changing US trade policies.

Competitive Positioning Against Other Markets

The UAE’s tax framework now offers several advantages compared to alternative investment destinations:

| Feature | UAE | Singapore | UK | US |

|---|---|---|---|---|

| Corporate Tax Rate for Qualifying Funds | 0% | Variable rates with exemptions | Up to 25% | Up to 21% federal + state taxes |

| Real Estate Investment Allowance | <10% for tax exemption | No specific threshold | No blanket exemption | REITs have specific tax structure |

| Ownership Breach Grace Period | 90 days | Limited flexibility | Varies by structure | Strict compliance required |

| Registration Requirements | Simplified for qualifying funds | Multiple registrations | Complex reporting | Extensive disclosure |

| Market Stability Rating | High | High | Moderate | Fluctuating |

Source: JobXDubai Financial Analysis, April 2025

The UAE’s approach combines substantive tax benefits with procedural simplicity, creating a particularly attractive proposition for institutional investors seeking both returns and administrative efficiency.

Strategic Timing: Tax Benefits in the Trump Era

The timing of these regulatory updates is particularly significant given the changing global trade landscape under the second Trump administration.

Global Context for UAE’s Tax Positioning

Several factors make these changes especially relevant:

- US tariff implications: New American trade policies creating investment uncertainty

- Capital flow redirection: International investors seeking stable alternatives

- Regulatory predictability: UAE offering clear guidelines amid global volatility

- Institutional investment targeting: Structured approach to attracting sophisticated investors

By introducing these changes now, the UAE demonstrates responsiveness to market conditions while reinforcing its position as a stable investment destination amid global uncertainty.

Market Impact: Investment Categories Likely to Benefit

Certain investment categories stand to benefit particularly from these regulatory updates, presenting opportunities for strategic portfolio adjustments.

Sectors Positioned for Growth

Based on the new tax framework, these investment categories may see increased foreign participation:

- Technology venture funds with limited real estate exposure

- Financial service investment vehicles targeting UAE expansion

- Manufacturing and logistics sector funds supporting economic diversification

- Healthcare and education investment platforms in high-growth segments

- REITs focusing on commercial and institutional properties with strong distribution policies

The exemption for funds with minimal real estate exposure particularly favors technology and service-sector investments, aligning with the UAE’s economic diversification objectives.

Implementation Timeline and Compliance Requirements

Understanding the practical application of these tax updates is essential for investment planning and compliance management.

Key Dates and Procedural Requirements

Foreign investors should note these important timeline elements:

- Immediate effect: The updated regulations are already in force

- Registration timing: For REITs, registration requirement only triggered at dividend distribution

- Assessment period: Two-year grace period for ownership structure compliance

- Remediation window: 90-day period to address any subsequent breaches

- Distribution timeline: Nine-month post-financial year window for REIT income distribution to qualify

These timeline provisions offer operational flexibility while maintaining the integrity of the tax framework, allowing investors to plan effectively.

Strategic Recommendations for Foreign Investors

Given these regulatory updates, foreign investors should consider several strategic approaches to maximize benefits under the new framework.

Action Steps for 2025

To optimize investment positioning under the updated tax rules:

- Review current fund structures against qualifying criteria for exemption

- Assess real estate exposure within investment portfolios (target below 10%)

- Evaluate ownership distribution to ensure compliance with percentage thresholds

- Structure new investments to align with exemption criteria from inception

- Consider REIT investments with strong distribution policies

- Implement compliance monitoring to identify potential breaches early

- Consult with UAE tax specialists for structure-specific guidance

“For institutional investors, these changes present an opportunity to reconfigure investment approaches to maximize tax efficiency while maintaining desired market exposure,” advises a Dubai-based financial consultant. “The clarity provided by these updates significantly reduces uncertainty in investment planning.”

Conclusion: UAE’s Tax Framework as a Strategic Asset

The UAE’s updated corporate tax framework for foreign investors represents more than regulatory adjustment—it constitutes a strategic positioning of the Emirates as a premier destination for global capital in uncertain times. By providing clear guidelines, substantive exemptions, and operational flexibility, these changes reinforce Dubai’s reputation as both a sophisticated financial center and a stable investment environment.

For foreign investors navigating complex global markets, the UAE’s approach offers a compelling combination of tax efficiency and procedural clarity. As international capital flows adjust to changing trade policies and economic conditions, the Emirates’ updated framework provides both immediate benefits and long-term strategic advantages.

To fully leverage these opportunities, investors should work with qualified advisors to evaluate existing structures and optimize new investments in alignment with the updated regulations. By doing so, they can capture the full benefit of the UAE’s increasingly attractive position in the global investment landscape.

Leave a comment